Page 103 - MA-12

P. 103

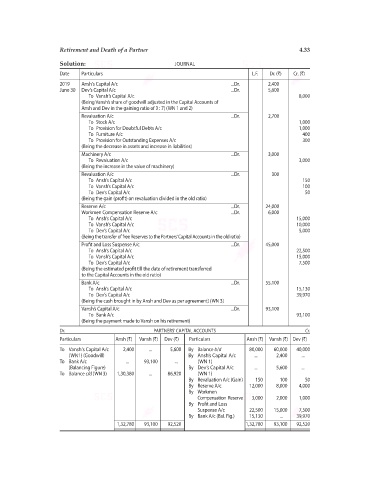

Retirement and Death of a Partner 4.33

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2019 Ansh’s Capital A/c ...Dr. 2,400

June 30 Dev’s Capital A/c ...Dr. 5,600

To Vansh’s Capital A/c 8,000

(Being Vansh’s share of goodwill adjusted in the Capital Accounts of

Ansh and Dev in the gaining ratio of 3 : 7) (WN 1 and 2)

Revaluation A/c ...Dr. 2,700

To Stock A/c 1,000

To Provision for Doubtful Debts A/c 1,000

To Furniture A/c 400

To Provision for Outstanding Expenses A/c 300

(Being the decrease in assets and increase in liabilities)

Machinery A/c ...Dr. 3,000

To Revaluation A/c 3,000

(Being the increase in the value of machinery)

Revaluation A/c ...Dr. 300

To Ansh’s Capital A/c 150

To Vansh’s Capital A/c 100

To Dev’s Capital A/c 50

(Being the gain (profit) on revaluation divided in the old ratio)

Reserve A/c ...Dr. 24,000

Workmen Compensation Reserve A/c ...Dr. 6,000

To Ansh’s Capital A/c 15,000

To Vansh’s Capital A/c 10,000

To Dev’s Capital A/c 5,000

(Being the transfer of free Reserves to the Partners’ Capital Accounts in the old ratio)

Profit and Loss Suspense A/c ...Dr. 45,000

To Ansh’s Capital A/c 22,500

To Vansh’s Capital A/c 15,000

To Dev’s Capital A/c 7,500

(Being the estimated profit till the date of retirement transferred

to the Capital Accounts in the old ratio)

Bank A/c ...Dr. 55,100

To Ansh’s Capital A/c 15,130

To Dev’s Capital A/c 39,970

(Being the cash brought in by Ansh and Dev as per agreement) (WN 3)

Vansh’s Capital A/c ...Dr. 93,100

To Bank A/c 93,100

(Being the payment made to Vansh on his retirement)

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Ansh (`) Vansh (`) Dev (`) Particulars Ansh (`) Vansh (`) Dev (`)

To Vansh’s Capital A/c 2,400 ... 5,600 By Balance b/d 80,000 60,000 40,000

(WN1) (Goodwill) By Ansh’s Capital A/c ... 2,400 ...

To Bank A/c ... 93,100 ... (WN 1)

(Balancing Figure) By Dev’s Capital A/c ... 5,600 ...

To Balance c/d (WN 3) 1,30,380 ... 86,920 (WN 1)

By Revaluation A/c (Gain) 150 100 50

By Reserve A/c 12,000 8,000 4,000

By Workmen

Compensation Reserve 3,000 2,000 1,000

By Profit and Loss

Suspense A/c 22,500 15,000 7,500

By Bank A/c (Bal. Fig.) 15,130 ... 39,970

1,32,780 93,100 92,520 1,32,780 93,100 92,520