Page 317 - MA-12

P. 317

M.8 Management Accounting (Section B)—ISC XII

Answers

1. (i) When a company purchases its own debentures in the open market for the purpose

of cancellation, such an act of purchasing and cancelling the debentures is known

as redemption by purchase of debentures in the open market.

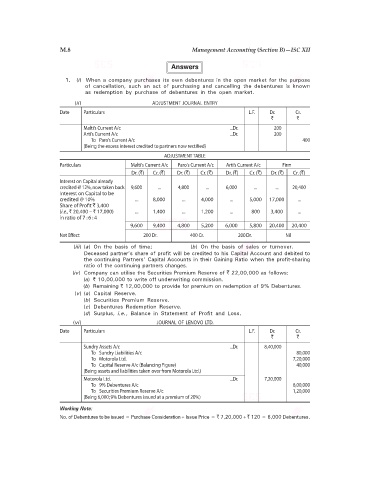

(ii) ADJUSTMENT JOURNAL ENTRY

Date Particulars L.F. Dr. Cr.

` `

Malti’s Current A/c ...Dr. 200

Arti’s Current A/c ...Dr. 200

To Paro’s Current A/c 400

(Being the excess interest credited to partners now rectified)

ADJUSTMENT TABLE

Particulars Malti‘s Current A/c Paro‘s Current A/c Arti’s Current A/c Firm

Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`)

Interest on Capital already

credited @ 12%, now taken back 9,600 ... 4,800 ... 6,000 ... ... 20,400

Interest on Capital to be

credited @ 10% ... 8,000 ... 4,000 ... 5,000 17,000 ...

Share of Profit ` 3,400

(i.e., ` 20,400 – ` 17,000) ... 1,400 ... 1,200 ... 800 3,400 ...

in ratio of 7 : 6 : 4

9,600 9,400 4,800 5,200 6,000 5,800 20,400 20,400

Net Effect 200 Dr. 400 Cr. 200 Dr. Nil

(iii) (a) On the basis of time; (b) On the basis of sales or turnover.

Deceased partner’s share of profit will be credited to his Capital Account and debited to

the continuing Partners’ Capital Accounts in their Gaining Ratio when the profit-sharing

ratio of the continuing partners changes.

(iv) Company can utilise the Securities Premium Reserve of ` 22,00,000 as follows:

(a) ` 10,00,000 to write off underwriting commission.

(b) Remaining ` 12,00,000 to provide for premium on redemption of 9% Debentures.

(v) (a) Capital Reserve.

(b) Securities Premium Reserve.

(c) Debentures Redemption Reserve.

(d) Surplus, i.e., Balance in Statement of Profit and Loss.

(vi) JOURNAL OF LENOVO LTD.

Date Particulars L.F. Dr. Cr.

` `

Sundry Assets A/c ...Dr. 8,40,000

To Sundry Liabilities A/c 80,000

To Motorola Ltd. 7,20,000

To Capital Reserve A/c (Balancing Figure) 40,000

(Being assets and liabilities taken over from Motorola Ltd.)

Motorola Ltd. ...Dr. 7,20,000

To 9% Debentures A/c 6,00,000

To Securities Premium Reserve A/c 1,20,000

(Being 6,000; 9% Debentures issued at a premium of 20%)

Working Note:

No. of Debentures to be issued = Purchase Consideration ÷ Issue Price = ` 7,20,000 ÷ ` 120 = 6,000 Debentures.