Page 14 - AAAXII

P. 14

Model Test Papers M.11

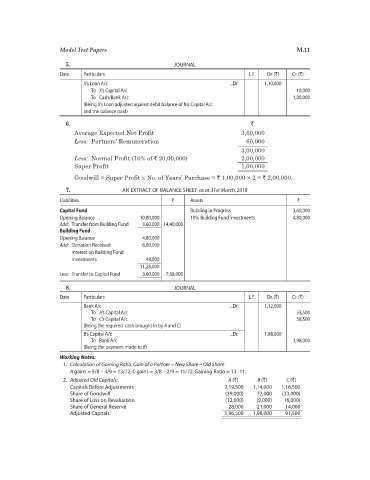

5. JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

X’s Loan A/c ...Dr. 1,10,000

To X’s Capital A/c 10,000

To Cash/Bank A/c 1,00,000

(Being X’s Loan adjusted against debit balance of his Capital A/c

and the balance paid)

6. `

Average Expected Net Profit 3,60,000

Less: Partners’ Remuneration 60,000

3,00,000

Less: Normal Profit (10% of ` 20,00,000) 2,00,000

Super Profit 1,00,000

Goodwill = Super Profit × No. of Years’ Purchase = ` 1,00,000 × 2 = ` 2,00,000.

7. AN EXTRACT OF BALANCE SHEET as at 31st March, 2018

Liabilities ` Assets `

Capital Fund Building in Progress 3,60,000

Opening Balance 10,80,000 10% Building Fund Investments 4,80,000

Add: Transfer from Building Fund 3,60,000 14,40,000

Building Fund

Opening Balance 4,80,000

Add: Donation Received 6,00,000

Interest on Building Fund

Investments 48,000

11,28,000

Less: Transfer to Capital Fund 3,60,000 7,68,000

8. JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

Bank A/c ...Dr. 1,12,000

To A’s Capital A/c 53,500

To C’s Capital A/c 58,500

(Being the required cash brought in by A and C)

B’s Capital A/c ...Dr. 1,98,000

To Bank A/c 1,98,000

(Being the payment made to B)

Working Notes:

1. Calculation of Gaining Ratio: Gain of a Partner = New Share – Old Share

A gains = 5/8 – 4/9 = 13/72; C gains = 3/8 – 2/9 = 11/72. Gaining Ratio = 13 : 11.

2. Adjusted Old Capitals: A (`) B (`) C (`)

Capitals Before Adjustments 2,19,500 1,14,000 1,16,500

Share of Goodwill (39,000) 72,000 (33,000)

Share of Loss on Revaluation (12,000) (9,000) (6,000)

Share of General Reserve 28,000 21,000 14,000

Adjusted Capitals 1,96,500 1,98,000 91,500