Page 230 - AAAXII

P. 230

Model Test Papers M.219

2. Calculation of Gaining Ratio:

Gain of a partner = New share – Old share

4 – 1 3

Ram’s Gain = 1/2 – 4/8 = Nil; Vrinda’s Gain = 1/2 – 1/8 = =

8 8

Hence, only Vrinda is gaining partner.

3. Calculation of Ghanshyam’s share of profit till the date of death:

` 40,000 + ` 80,000

Average profit of past two years = = ` 60,000

2

Profit for 10 months (from 1st April, 2014 to 1st February, 2015) = ` 60,000 × 10/12 = ` 50,000

Ghanshyam’s share of profit = ` 50,000 × 3/8 = ` 18,750.

Due to change in profit-sharing ratio in the new firm, Ghanshyam’s share of profit will be adjusted through

Vrinda’s Capital Account (gaining partner) not through Profit and Loss Suspense Account.

(b) A partner may retire:

(i) with the consent of all other partners.

(ii) in accordance with an agreement among the partners.

(iii) by giving notice in writing, to all other partners of his intention to retire in case

Partnership is ‘Partnership at Will’.

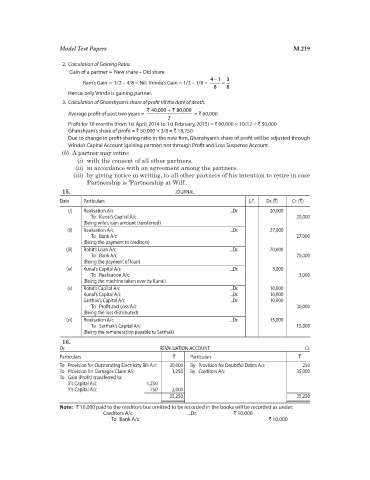

15. JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

(i) Realisation A/c ...Dr. 20,000

To Kunal’s Capital A/c 20,000

(Being wife’s loan amount transferred)

(ii) Realisation A/c ...Dr. 27,000

To Bank A/c 27,000

(Being the payment to creditors)

(iii) Rohit’s Loan A/c ...Dr. 70,000

To Bank A/c 70,000

(Being the payment of loan)

(iv) Kunal’s Capital A/c ...Dr. 3,000

To Realisation A/c 3,000

(Being the machine taken over by Kunal)

(v) Rohit’s Capital A/c ...Dr. 10,000

Kunal’s Capital A/c ...Dr. 10,000

Sarthak’s Capital A/c ..Dr. 10,000

To Profit and Loss A/c 30,000

(Being the loss distributed)

(vi) Realisation A/c ...Dr. 15,000

To Sarthak’s Capital A/c 15,000

(Being the remuneration payable to Sarthak)

16.

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Provision for Outstanding Electricity Bill A/c 30,000 By Provision for Doubtful Debts A/c 250

To Provision for Damages Claim A/c 3,250 By Creditors A/c 35,000

To Gain (Profit) transferred to:

X’s Capital A/c 1,250

Y’s Capital A/c 750 2,000

35,250 35,250

Note: ` 10,000 paid to the creditors but omitted to be recorded in the books will be recorded as under:

Creditors A/c ...Dr. ` 10,000

To Bank A/c ` 10,000