Page 50 - afs12

P. 50

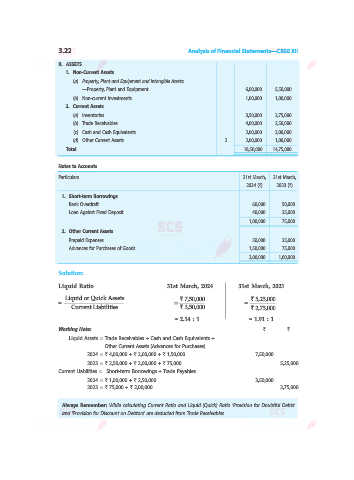

4.4 Analysis of Financial Statements—CBSE XII

Total Assets has the same meaning as in Total Assets to Debt Ratio.

Profit before Interest and Tax = Profit after Tax + Tax + Interest.

Shareholders’ Funds = Share Capital + Reserves and Surplus.

Debt means Long-term Debts, i.e., Non-current Liabilities. Capital Employed = Shareholders’ Funds + Long-term Debts. Average Inventory Opening Inventory + Closing Inventory 2 Trade Receivables means debtors plus bills receivable. Provision for Doubtful Debts is not deducted. Average Trade Receivables (Opening Debtors + Opening Bills Receivable) + btors + Closing Bills Receivable) (Closing Deb 2 Trade Payables means creditors plus

Pure Ratio or % Times Pure Ratio Times = Times Times Times Times

This ratio shows the extent to which total assets have been financed by the proprietor. Higher the ratio, higher the safety margin for unsecured lenders and creditors. This ratio shows how many times the interest charges are covered by the profits available to pay interest. Higher the ratio, more security for the lender is in respect of payment of interest regularly. This ratio shows the amount of Long-term Debts in Capital Employed. Low ratio means more

Funds or sets beforeInterest andTax Trade Receivables Turnover Ratio Credit Revenue from AverageTradeReceivables early payments. of fixed assets.

Proprietary Ratio Shareholders’ ’ = Proprietors Funds or Equity Total Ass Interest Coverage Ratio Profit Interest on Long-term Debt Debt to Capital Employed Ratio Long-term Debt = Capital Employed Inventory Turnover Ratio Cost of Revenue from Operations Average Inventory Operations Trade Payables Turnover Ratio NetCreditPurchases AverageTradePayables Working Capital Turnover Ratio = Revenuefrom Operations WorkingCapital Fixed Assets Turn

3. 4. 5. 1. = 2. = 3. = 4. 5. =