Page 73 - DEBK11

P. 73

11.2 Double Entry Book Keeping—CBSE XI

• Purchases Book is a book of primary entry, used for recording credit purchases of goods,

i.e., goods in which the firm deals or uses for manufacturing goods. Cash purchases are not

recorded in the Purchases Book. They are recorded in the Cash Book.

• Sales Book is used for the purposes of recording the sale of merchandise on credit.

• Purchases Return Book (also known as Returns Outward Book) is used for recording

all return of goods purchased.

• Sales Return Book (also known as Returns Inward Book) is used for the purposes of

recording the return of goods sold.

• Journal Proper is used for making the original record of those transactions which do not

find a place in any other subsidiary book. Entries recorded in the Journal Proper are:

(i) Opening Entry; (ii) Closing Entry; (iii) Transfer Entries; (iv) Credit Purchase of Assets;

(v) Rectifying Entries; (vi) Adjustment Entries; (vii) Credit Sale of Worn-out or Obsolete Assets.

Solved Question

1. Enter the following transactions in various Subsidiary Books and post them into

Ledger and prepare a Trial Balance:

2025

April 1 Cash in hand ` 1,00,000; Cash at Bank ` 75,000 and Capital Account ` 1,75,000.

April 3 Bought goods for cash ` 45,000.

April 4 Purchased goods from Pradeep & Co. ` 20,000 less 10% trade discount.

April 7 Sold goods to Dheeraj & Co. for ` 20,000 less 20% trade discount.

April 9 Withdrew ` 5,000 from bank for personal use.

April 12 Sold goods to Dhruv for ` 15,000.

April 15 Paid ` 17,800 to Pradeep & Co. in full settlement of their account.

April 18 Goods of ` 2,000 returned by Dhruv.

April 20 Received ` 5,000 from Dhruv.

April 21 Purchased goods from KG & Co. ` 25,000.

April 23 ` 20,600 paid to KG & Co. by cheque, discount received ` 400.

April 24 Purchased furniture of ` 20,000 from Modern Furniture House.

April 26 Paid into bank ` 5,000.

April 28 Dhruv is declared insolvent; a first and final dividend of 50 paise in a rupee is received from him.

April 29 Goods costing ` 3,000 returned to KG & Co.

April 30 Goods costing ` 5,000 taken by the proprietor.

April 30 Interest on Capital provided ` 1,000.

April 30 Paid ` 10,000 for advertisement by cheque.

April 30 Paid Salaries to staff ` 10,000.

April 30 Cash Sales ` 15,000.

April 30 Paid into bank ` 15,000.

April 30 Bought 100 shares of a company at ` 10 per share; brokerage paid ` 50.

April 30 Received ` 14,800 from Dheeraj & Co., discount allowed ` 200.

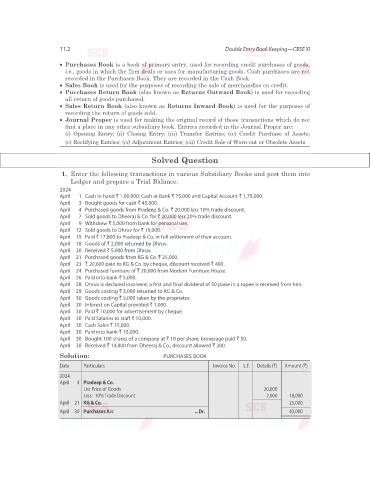

Solution: PURCHASES BOOK

Date Particulars Invoice No. L.F. Details (`) Amount (`)

2025

April 4 Pradeep & Co.

List Price of Goods 20,000

Less: 10% Trade Discount 2,000 18,000

April 21 KG & Co. 25,000

April 30 Purchases A/c ...Dr. 43,000