Page 132 - ISCDEBK-XI

P. 132

Depreciation 15.17

2. Calculation of Profit on Sale of Machinery on 31st August, 2015: `

Cost on 1st April, 2012 (` 30,000 + ` 1,500) 31,500

Less: Depreciation for 2012–13 4,725

Book Value on 1st April, 2013 26,775

Less: Depreciation for 2013–14 4,016

Book Value on 1st April, 2014 22,759

Less: Depreciation for 2014–15 3,414

Book Value on 1st April, 2015 19,345

Less: Depreciation for 5 Months (` 19,345 × 5/12 × 15/100) 1,209

Book Value on 31st August, 2015 18,136

Less: Amount realised on sale 36,000

Gain (Profit) on Sale of Machinery 17,864

3. Calculation of Loss on Sale of Machinery on 1st November, 2016: `

Book Value on 1st April, 2013 10,000

Less: Depreciation for 2013–14 1,500

Book Value on 1st April, 2014 8,500

Less: Depreciation for 2014–15 1,275

Book Value on 1st April, 2015 7,225

Less: Depreciation for 2015–16 1,084

Book Value on 1st April, 2016 6,141

Less: Depreciation for 7 months (` 6,141 × 7/12 × 15/100) 537

Book Value on 1st November, 2016 5,604

Less: Amount realised on Sale 4,000

Loss on Sale of Machinery 1,604

Illustration 12.

A firm imported a machine on 1st October, 2016 for ` 2,00,000, paid custom duty and

freight ` 40,000 and incurred erection charges ` 60,000. Another machinery costing

` 1,00,000 was purchased from the local market on 1st April, 2017. On 1st October, 2018,

one-third of the imported machinery got out of order and was sold for ` 40,000. Another

machinery was purchased to replace the same for ` 50,000 on the same date. Depreciation is

to be charged at 20% per annum on the cost following Straight Line Method.

Accounts are closed each year on 31st March. You are required to show:

(i) Machinery Account for 2016–17, 2017–18 and 2018–19.

(ii) Machinery Account and Provision for Depreciation Account for 2016–17, 2017–18 and

2018–19.

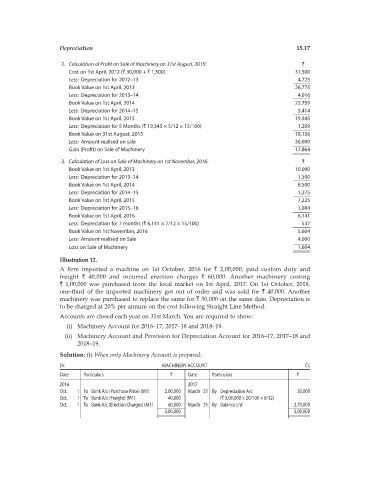

Solution: (i) When only Machinery Account is prepared:

Dr. MACHINERY ACCOUNT Cr.

Date Particulars ` Date Particulars `

2016 2017

Oct. 1 To Bank A/c (Purchase Price) (M1) 2,00,000 March 31 By Depreciation A/c 30,000

Oct. 1 To Bank A/c (Freight) (M1) 40,000 (` 3,00,000 × 20/100 × 6/12)

Oct. 1 To Bank A/c (Erection Charges) (M1) 60,000 March 31 By Balance c/d 2,70,000

3,00,000 3,00,000