Page 228 - ISCDEBK-XI

P. 228

21.16 Double Entry Book Keeping—ISC XI

Creditor’s A/c ...Dr. 5,000

To Cash A/c 4,800

To Discount Received A/c 200

(Being cash paid to a creditor and discount allowed by him omitted

to be recorded, now recorded)

Cashier’s A/c ...Dr. 25,200

To Cash A/c 25,200

(Being cash defaulted by the cashier)

Dr. SUSPENSE ACCOUNT Cr.

Particulars ` Particulars `

To Discount Received A/c 100 By Difference in Books as per Trial Balance 1,210

To Merchant’s A/c 910 (Balancing Figure)

To Customer’s A/c 200

1,210 1,210

Note: Suspense Account indicates that there was a difference of ` 1,210 in the Trial Balance before deducting

the errors. Debit side of the Trial Balance exceeded credit side by ` 1,210.

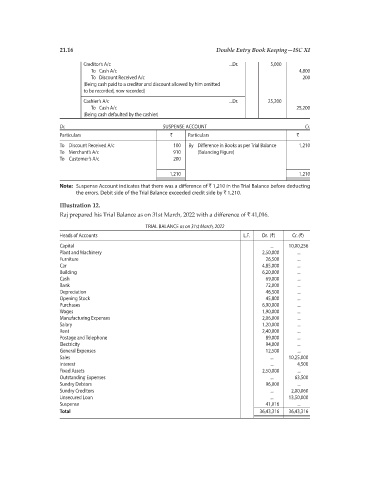

Illustration 12.

Raj prepared his Trial Balance as on 31st March, 2022 with a difference of ` 41,016.

TRIAL BALANCE as on 31st March, 2022

Heads of Accounts L.F. Dr. (`) Cr. (`)

Capital ... 10,00,256

Plant and Machinery 2,50,000 ...

Furniture 26,500 ...

Car 4,85,000 ...

Building 6,20,000 ...

Cash 69,000 ...

Bank 72,000 ...

Depreciation 46,500 ...

Opening Stock 45,800 ...

Purchases 6,90,000 ...

Wages 1,90,000 ...

Manufacturing Expenses 2,06,000 ...

Salary 1,20,000 ...

Rent 2,40,000 ...

Postage and Telephone 89,000 ...

Electricity 94,000 ...

General Expenses 12,500 ...

Sales ... 10,25,000

Interest ... 4,500

Fixed Assets 2,50,000 ...

Outstanding Expenses ... 63,500

Sundry Debtors 96,000 ...

Sundry Creditors ... 2,00,060

Unsecured Loan ... 13,50,000

Suspense 41,016 ...

Total 36,43,316 36,43,316