Page 102 - ISCDEBK-12

P. 102

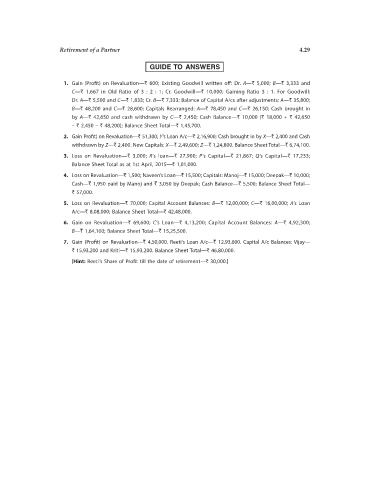

Retirement of a Partner 4.29

GUIDE TO ANSWERS

1. Gain (Profit) on Revaluation—` 600; Existing Goodwill written off: Dr. A—` 5,000; B—` 3,333 and

C—` 1,667 in Old Ratio of 3 : 2 : 1; Cr. Goodwill—` 10,000; Gaining Ratio 3 : 1. For Goodwill:

Dr. A—` 5,500 and C—` 1,833; Cr. B—` 7,333; Balance of Capital A/cs after adjustments: A—` 35,800;

B—` 48,200 and C—` 28,600; Capitals Rearranged: A—` 78,450 and C—` 26,150; Cash brought in

by A—` 42,650 and cash withdrawn by C—` 2,450; Cash Balance—` 10,000 (` 18,000 + ` 42,650

– ` 2,450 – ` 48,200); Balance Sheet Total—` 1,45,700.

2. Gain Profit) on Revaluation—` 51,300; Y’s Loan A/c—` 2,16,900; Cash brought in by X—` 2,400 and Cash

withdrawn by Z—` 2,400. New Capitals: X—` 2,49,600; Z—` 1,24,800. Balance Sheet Total—` 6,74,100.

3. Loss on Revaluation—` 3,000; R’s loan—` 27,900; P’s Capital—` 21,867; Q’s Capital—` 17,233;

Balance Sheet Total as at 1st April, 2015—` 1,01,000.

4. Loss on Revaluation—` 1,500; Naveen’s Loan—` 15,500; Capitals: Manoj—` 15,000; Deepak—` 10,000;

Cash—` 1,950 paid by Manoj and ` 3,050 by Deepak; Cash Balance—` 5,500; Balance Sheet Total—

` 57,000.

5. Loss on Revaluation—` 70,000; Capital Account Balances: B—` 12,00,000; C—` 16,00,000; A’s Loan

A/c—` 8,08,000; Balance Sheet Total—` 42,48,000.

6. Gain on Revaluation—` 69,600; C’s Loan—` 4,13,200; Capital Account Balances: A—` 4,92,300;

B—` 1,64,100; Balance Sheet Total—` 15,25,500.

7. Gain (Profit) on Revaluation—` 4,50,000. Reeti’s Loan A/c—` 12,93,600. Capital A/c Balances: Vijay—

` 15,93,200 and Kriti—` 15,93,200. Balance Sheet Total—` 46,80,000.

[Hint: Reeti’s Share of Profit till the date of retirement—` 30,000.]