Page 185 - ISCDEBK-12

P. 185

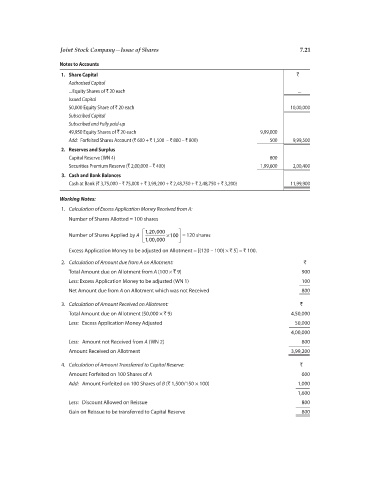

Joint Stock Company—Issue of Shares 7.21

Notes to Accounts

1. Share Capital `

Authorised Capital

... Equity Shares of ` 20 each ...

Issued Capital

50,000 Equity Share of ` 20 each 10,00,000

Subscribed Capital

Subscribed and Fully paid-up

49,950 Equity Shares of ` 20 each 9,99,000

Add: Forfeited Shares Account (` 600 + ` 1,500 – ` 800 – ` 800) 500 9,99,500

2. Reserves and Surplus

Capital Reserve (WN 4) 800

Securities Premium Reserve (` 2,00,000 – ` 400) 1,99,600 2,00,400

3. Cash and Bank Balances

Cash at Bank (` 3,75,000 – ` 75,000 + ` 3,99,200 + ` 2,48,750 + ` 2,48,750 + ` 3,200) 11,99,900

Working Notes:

1. Calculation of Excess Application Money Received from A:

Number of Shares Allotted = 100 shares

È 120 000 ˘

,

,

Number of Shares Applied by A Í ¥ 100 = 120 shares

˙

Î 100 000 ˚

,

,

Excess Application Money to be adjusted on Allotment = [(120 – 100) × ` 5] = ` 100.

2. Calculation of Amount due from A on Allotment: `

Total Amount due on Allotment from A (100 × ` 9) 900

Less: Excess Application Money to be adjusted (WN 1) 100

Net Amount due from A on Allotment which was not Received 800

3. Calculation of Amount Received on Allotment: `

Total Amount due on Allotment (50,000 × ` 9) 4,50,000

Less: Excess Application Money Adjusted 50,000

4,00,000

Less: Amount not Received from A (WN 2) 800

Amount Received on Allotment 3,99,200

4. Calculation of Amount Transferred to Capital Reserve: `

Amount Forfeited on 100 Shares of A 600

Add: Amount Forfeited on 100 Shares of B (` 1,500/150 × 100) 1,000

1,600

Less: Discount Allowed on Reissue 800

Gain on Reissue to be transferred to Capital Reserve 800