Page 27 - ISCDEBK-12

P. 27

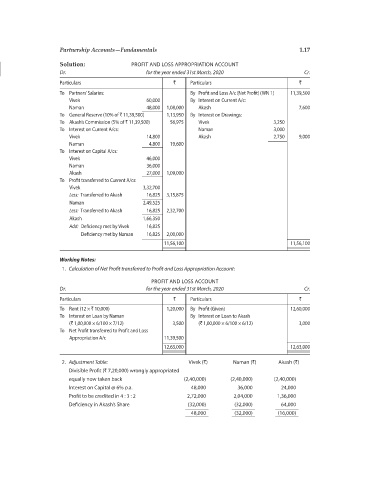

Partnership Accounts—Fundamentals 1.17

Solution: PROFIT AND LOSS APPROPRIATION ACCOUNT

Dr. for the year ended 31st March, 2020 Cr.

Particulars ` Particulars `

To Partners’ Salaries: By Profit and Loss A/c (Net Profit) (WN 1) 11,39,500

Vivek 60,000 By Interest on Current A/c:

Naman 48,000 1,08,000 Akash 7,600

To General Reserve (10% of ` 11,39,500) 1,13,950 By Interest on Drawings:

To Akash’s Commission (5% of ` 11,39,500) 56,975 Vivek 3,250

To Interest on Current A/cs: Naman 3,000

Vivek 14,800 Akash 2,750 9,000

Naman 4,800 19,600

To Interest on Capital A/cs:

Vivek 46,000

Naman 36,000

Akash 27,000 1,09,000

To Profit transferred to Current A/cs:

Vivek 3,32,700

Less: Transferred to Akash 16,825 3,15,875

Naman 2,49,525

Less: Transferred to Akash 16,825 2,32,700

Akash 1,66,350

Add: Deficiency met by Vivek 16,825

Deficiency met by Naman 16,825 2,00,000

11,56,100 11,56,100

Working Notes:

1. Calculation of Net Profit transferred to Profit and Loss Appropriation Account:

PROFIT AND LOSS ACCOUNT

Dr. for the year ended 31st March, 2020 Cr.

Particulars ` Particulars `

To Rent (12 × ` 10,000) 1,20,000 By Profit (Given) 12,60,000

To Interest on Loan by Naman By Interest on Loan to Akash

(` 1,00,000 × 6/100 × 7/12) 3,500 (` 1,00,000 × 6/100 × 6/12) 3,000

To Net Profit transferred to Profit and Loss

Appropriation A/c 11,39,500

12,63,000 12,63,000

2. Adjustment Table: Vivek (`) Naman (`) Akash (`)

Divisible Profit (` 7,20,000) wrongly appropriated

equally now taken back (2,40,000) (2,40,000) (2,40,000)

Interest on Capital @ 6% p.a. 48,000 36,000 24,000

Profit to be credited in 4 : 3 : 2 2,72,000 2,04,000 1,36,000

Deficiency in Akash’s Share (32,000) (32,000) 64,000

48,000 (32,000) (16,000)