Page 119 - MA-12

P. 119

Dissolution of a Partnership Firm 5.7

(v) (a) Realisation A/c ...Dr. 15,000

To Bank A/c 15,000

(Being the liability discharged)

(b) Workmen Compensation Reserve A/c ...Dr. 15,000

To X’s Capital A/c 6,000

To Y’s Capital A/c 6,000

To Z’s Capital A/c 3,000

(Being the transfer of excess workmen compensation reserve)

(vi) No Journal entry is required since there is no realisation.

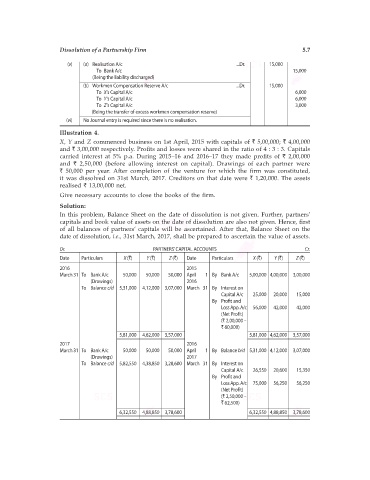

Illustration 4.

X, Y and Z commenced business on 1st April, 2015 with capitals of ` 5,00,000; ` 4,00,000

and ` 3,00,000 respectively. Profits and losses were shared in the ratio of 4 : 3 : 3. Capitals

carried interest at 5% p.a. During 2015–16 and 2016–17 they made profits of ` 2,00,000

and ` 2,50,000 (before allowing interest on capital). Drawings of each partner were

` 50,000 per year. After completion of the venture for which the firm was constituted,

it was dissolved on 31st March, 2017. Creditors on that date were ` 1,20,000. The assets

realised ` 13,00,000 net.

Give necessary accounts to close the books of the firm.

Solution:

In this problem, Balance Sheet on the date of dissolution is not given. Further, partners’

capitals and book value of assets on the date of dissolution are also not given. Hence, first

of all balances of partners’ capitals will be ascertained. After that, Balance Sheet on the

date of dissolution, i.e., 31st March, 2017, shall be prepared to ascertain the value of assets.

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Date Particulars X (`) Y (`) Z (`) Date Particulars X (`) Y (`) Z (`)

2016 2015

March 31 To Bank A/c 50,000 50,000 50,000 April 1 By Bank A/c 5,00,000 4,00,000 3,00,000

(Drawings) 2016

To Balance c/d 5,31,000 4,12,000 3,07,000 March 31 By Interest on

Capital A/c 25,000 20,000 15,000

By Profit and

Loss App. A/c 56,000 42,000 42,000

(Net Profit)

(` 2,00,000 –

` 60,000)

5,81,000 4,62,000 3,57,000 5,81,000 4,62,000 3,57,000

2017 2016

March 31 To Bank A/c 50,000 50,000 50,000 April 1 By Balance b/d 5,31,000 4,12,000 3,07,000

(Drawings) 2017

To Balance c/d 5,82,550 4,38,850 3,28,600 March 31 By Interest on

Capital A/c 26,550 20,600 15,350

By Profit and

Loss App. A/c 75,000 56,250 56,250

(Net Profit)

(` 2,50,000 –

` 62,500)

6,32,550 4,88,850 3,78,600 6,32,550 4,88,850 3,78,600