Page 175 - DEBKVOL-1

P. 175

Chapter 7 Death of a Partner 7.17

.

Due to an accident, Anil died on 1st October, 2018. Anil’s family became financially weak. Bhanu and Chandu

decided to admit Anil’s daughter in the business. It was agreed between Anil’s executors and the remaining

partners that:

(a) Goodwill to be valued at 2½ years’ purchase of the average profit of the previous four years which

were: Year 2014–15: ` 13,000; Year 2015–16: ` 12,000; Year 2016–17: ` 20,000; Year 2017–18: ` 15,000.

(b) Patents be valued at ` 8,000; Machinery at ` 28,000; and Building at ` 2,50,000.

(c) Profit for the year 2018–19 be taken as having accrued at the same rate as that of the previous year.

(d) Interest on capital be provided at 10% p.a.

(e) Half of the amount due to Anil be paid immediately.

Prepare Anil’s Capital Account and Anil’s Executors’ Account as on 1st October, 2018.

[Ans.: Anil’s Share of Goodwill—` 18,750; Anil’s Share of Profit—` 3,750. Amount Paid to

Anil’s Executors—` 39,750; Amount still payable to Anil’s Executors—` 39,750.]

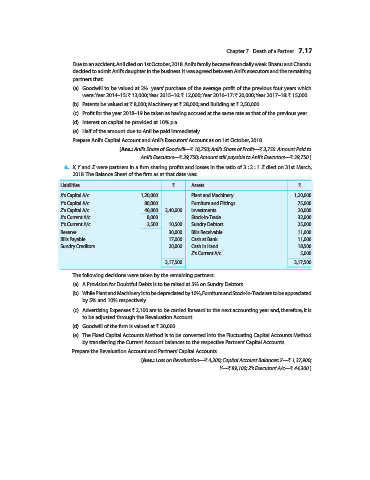

6. X, Y and Z were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Z died on 31st March,

2018. The Balance Sheet of the firm as at that date was:

Liabilities ` Assets `

X’s Capital A/c 1,20,000 Plant and Machinery 1,20,000

Y’s Capital A/c 80,000 Furniture and Fittings 75,000

Z’s Capital A/c 40,000 2,40,000 Investments 20,000

X’s Current A/c 8,000 Stock-in-Trade 32,000

Y’s Current A/c 2,500 10,500 Sundry Debtors 25,000

Reserve 30,000 Bills Receivable 11,000

Bills Payable 17,000 Cash at Bank 11,000

Sundry Creditors 20,000 Cash in Hand 18,500

Z’s Current A/c 5,000

3,17,500 3,17,500

The following decisions were taken by the remaining partners:

(a) A Provision for Doubtful Debts is to be raised at 5% on Sundry Debtors.

(b) While Plant and Machinery is to be depreciated by 10%, Furniture and Stock-in-Trade are to be appreciated

by 5% and 10% respectively.

(c) Advertising Expenses ` 2,100 are to be carried forward to the next accounting year and, therefore, it is

to be adjusted through the Revaluation Account.

(d) Goodwill of the firm is valued at ` 30,000.

(e) The Fixed Capital Accounts Method is to be converted into the Fluctuating Capital Accounts Method

by transferring the Current Account balances to the respective Partners’ Capital Accounts.

Prepare the Revaluation Account and Partners’ Capital Accounts.

[Ans.: Loss on Revaluation—` 4,200; Capital Account Balances: X—` 1,37,900;

Y—` 89,100; Z’s Executors’ A/c—` 44,300.]