Page 180 - DEBKVOL-1

P. 180

Chapter 8 Dissolution of a Partnership Firm 8.5

.

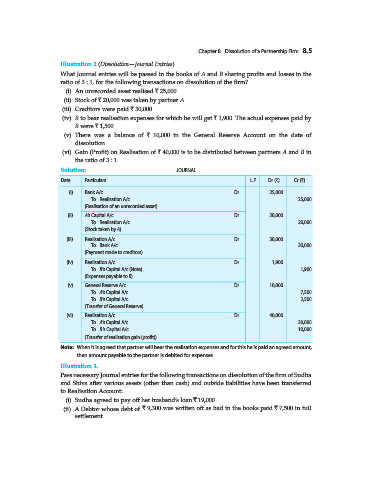

Illustration 2 (Dissolution—Journal Entries).

What Journal entries will be passed in the books of A and B sharing profits and losses in the

ratio of 3 : 1, for the following transactions on dissolution of the firm?

(i) An unrecorded asset realised ` 25,000.

(ii) Stock of ` 20,000 was taken by partner A.

(iii) Creditors were paid ` 30,000.

(iv) B to bear realisation expenses for which he will get ` 1,900. The actual expenses paid by

B were ` 1,500.

(v) There was a balance of ` 10,000 in the General Reserve Account on the date of

dissolution.

(vi) Gain (Profit) on Realisation of ` 40,000 is to be distributed between partners A and B in

the ratio of 3 : 1.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

(i) Bank A/c ...Dr. 25,000

To Realisation A/c 25,000

(Realisation of an unrecorded asset)

(ii) A’s Capital A/c ...Dr. 20,000

To Realisation A/c 20,000

(Stock taken by A)

(iii) Realisation A/c ...Dr. 30,000

To Bank A/c 30,000

(Payment made to creditors)

(iv) Realisation A/c ...Dr. 1,900

To B’s Capital A/c (Note) 1,900

(Expenses payable to B)

(v) General Reserve A/c ...Dr. 10,000

To A’s Capital A/c 7,500

To B’s Capital A/c 2,500

(Transfer of General Reserve)

(vi) Realisation A/c ...Dr. 40,000

To A’s Capital A/c 30,000

To B’s Capital A/c 10,000

(Transfer of realisation gain (profit))

Note: When it is agreed that partner will bear the realisation expenses and for this he is paid an agreed amount,

then amount payable to the partner is debited for expenses.

Illustration 3.

Pass necessary Journal entries for the following transactions on dissolution of the firm of Sudha

and Shiva after various assets (other than cash) and outside liabilities have been transferred

to Realisation Account:

(i) Sudha agreed to pay off her husband’s loan ` 19,000.

(ii) A Debtor whose debt of ` 9,300 was written off as bad in the books paid ` 7,500 in full

settlement.