Page 68 - DEBKVOL-1

P. 68

3.10 Double Entry Book Keeping—CBSE XII

8. A firm earns ` 3,00,000 as its annual profit, the rate of return being 12%. Assets and liabilities of the

firm amounted to ` 36,00,000 and ` 12,00,000 respectively. Calculate value of goodwill by Capitalisation

Method. [Ans.: Goodwill—` 1,00,000.]

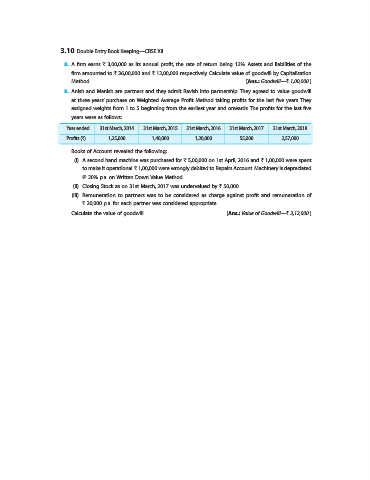

9. Anish and Manish are partners and they admit Ravish into partnership. They agreed to value goodwill

at three years’ purchase on Weighted Average Profit Method taking profits for the last five years. They

assigned weights from 1 to 5 beginning from the earliest year and onwards. The profits for the last five

years were as follows:

Year ended 31st March, 2014 31st March, 2015 31st March, 2016 31st March, 2017 31st March, 2018

Profits (`) 1,25,000 1,40,000 1,20,000 55,000 2,57,000

Books of Account revealed the following:

(i) A second hand machine was purchased for ` 5,00,000 on 1st April, 2016 and ` 1,00,000 were spent

to make it operational. ` 1,00,000 were wrongly debited to Repairs Account. Machinery is depreciated

@ 20% p.a. on Written Down Value Method.

(ii) Closing Stock as on 31st March, 2017 was undervalued by ` 50,000.

(iii) Remuneration to partners was to be considered as charge against profit and remuneration of

` 20,000 p.a. for each partner was considered appropriate.

Calculate the value of goodwill. [Ans.: Value of Goodwill—` 3,12,000.]