Page 71 - DEBKVOL-1

P. 71

Chapter 4 Change in Profit-Sharing Ratio Among the Existing Partners 4.3

.

Solved Questions

Illustration 1.

Following is the Balance Sheet of X, Y and Z, who share profits and losses in the ratio of

2 : 3 : 1 as at 31st March, 2018:

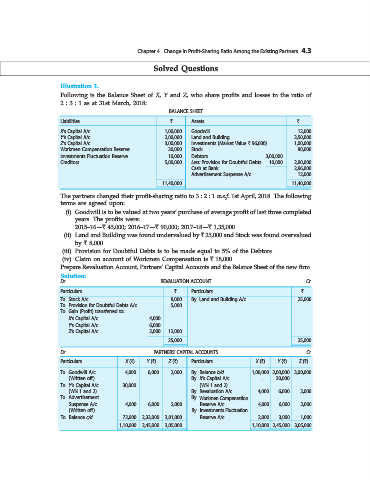

BALANCE SHEET

Liabilities ` Assets `

X’s Capital A/c 1,00,000 Goodwill 12,000

Y’s Capital A/c 2,00,000 Land and Building 3,50,000

Z’s Capital A/c 3,00,000 Investments (Market Value ` 96,000) 1,00,000

Workmen Compensation Reserve 30,000 Stock 80,000

Investments Fluctuation Reserve 10,000 Debtors 3,00,000

Creditors 5,00,000 Less: Provision for Doubtful Debts 10,000 2,90,000

Cash at Bank 2,96,000

Advertisement Suspense A/c 12,000

11,40,000 11,40,000

The partners changed their profit-sharing ratio to 3 : 2 : 1 w.e.f. 1st April, 2018. The following

terms are agreed upon:

(i) Goodwill is to be valued at two years’ purchase of average profit of last three completed

years. The profits were:

2015–16—` 45,000; 2016–17—` 90,000; 2017–18—` 1,35,000.

(ii) Land and Building was found undervalued by ` 25,000 and Stock was found overvalued

by ` 8,000.

(iii) Provision for Doubtful Debts is to be made equal to 5% of the Debtors.

(iv) Claim on account of Workmen Compensation is ` 18,000.

Prepare Revaluation Account, Partners’ Capital Accounts and the Balance Sheet of the new firm.

Solution:

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Stock A/c 8,000 By Land and Building A/c 25,000

To Provision for Doubtful Debts A/c 5,000

To Gain (Profit) transferred to:

X’s Capital A/c 4,000

Y’s Capital A/c 6,000

Z’s Capital A/c 2,000 12,000

25,000 25,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X (`) Y (`) Z (`) Particulars X (`) Y (`) Z (`)

To Goodwill A/c 4,000 6,000 2,000 By Balance b/d 1,00,000 2,00,000 3,00,000

(Written off) By X’s Capital A/c ... 30,000 ...

To Y’s Capital A/c 30,000 ... ... (WN 1 and 2)

(WN 1 and 2) By Revaluation A/c 4,000 6,000 2,000

To Advertisement By Workmen Compensation

Suspense A/c 4,000 6,000 2,000 Reserve A/c 4,000 6,000 2,000

(Written off) By Investments Fluctuation

To Balance c/d 72,000 2,33,000 3,01,000 Reserve A/c 2,000 3,000 1,000

1,10,000 2,45,000 3,05,000 1,10,000 2,45,000 3,05,000