Page 146 - AAAXII

P. 146

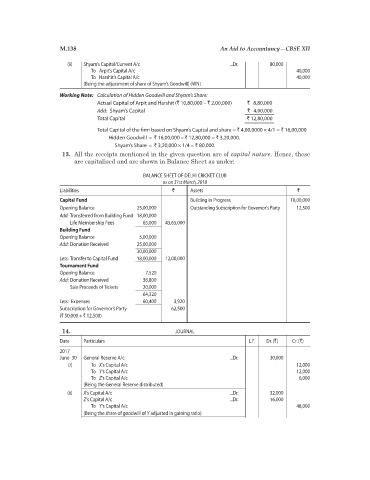

M.138 An Aid to Accountancy—CBSE XII

(ii) Shyam’s Capital/Current A/c ...Dr. 80,000

To Arpit’s Capital A/c 40,000

To Harshit’s Capital A/c 40,000

(Being the adjustment of share of Shyam’s Goodwill) (WN)

Working Note: Calculation of Hidden Goodwill and Shyam’s Share:

Actual Capital of Arpit and Harshit (` 10,80,000 – ` 2,00,000) ` 8,80,000

Add: Shyam’s Capital ` 4,00,000

Total Capital ` 12,80,000

Total Capital of the firm based on Shyam’s Capital and share = ` 4,00,0000 × 4/1 = ` 16,00,000

Hidden Goodwill = ` 16,00,000 – ` 12,80,000 = ` 3,20,000.

Shyam’s Share = ` 3,20,000 × 1/4 = ` 80,000.

13. All the receipts mentioned in the given question are of capital nature. Hence, these

are capitalised and are shown in Balance Sheet as under:

BALANCE SHEET OF DELHI CRICKET CLUB

as on 31st March, 2018

Liabilities ` Assets `

Capital Fund Building in Progress 18,00,000

Opening Balance 25,00,000 Outstanding Subscription for Governor’s Party 12,500

Add: Transferred from Building Fund 18,00,000

Life Membership Fees 65,000 43,65,000

Building Fund

Opening Balance 5,00,000

Add: Donation Received 25,00,000

30,00,000

Less: Transfer to Capital Fund 18,00,000 12,00,000

Tournament Fund

Opening Balance 7,520

Add: Donation Received 36,800

Sale Proceeds of Tickets 20,000

64,320

Less: Expenses 60,400 3,920

Subscription for Governor’s Party 62,500

(` 50,000 + ` 12,500)

14. JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2017

June 30 General Reserve A/c ...Dr. 30,000

(i) To X’s Capital A/c 12,000

To Y’s Capital A/c 12,000

To Z’s Capital A/c 6,000

(Being the General Reserve distributed)

(ii) X’s Capital A/c ...Dr. 32,000

Z’s Capital A/c ...Dr. 16,000

To Y’s Capital A/c 48,000

(Being the share of goodwill of Y adjusted in gaining ratio)