Page 154 - AAAXII

P. 154

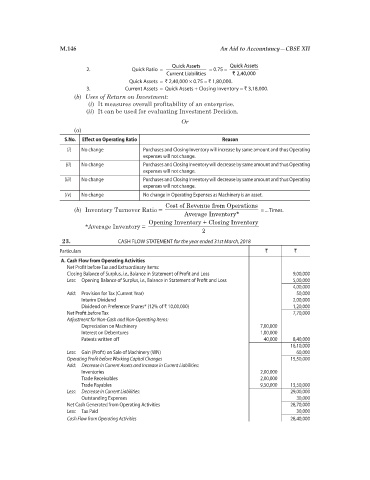

M.146 An Aid to Accountancy—CBSE XII

Quick Assets Quick Assets

2. Quick Ratio = = 0.75 =

Current Liabilities ` 2,40,000

Quick Assets = ` 2,40,000 × 0.75 = ` 1,80,000.

3. Current Assets = Quick Assets + Closing Inventory = ` 3,18,000.

(b) Uses of Return on Investment:

(i) It measures overall profitability of an enterprise.

(ii) It can be used for evaluating Investment Decision.

Or

(a)

S.No. Effect on Operating Ratio Reason

(i) No change Purchases and Closing Inventory will increase by same amount and thus Operating

expenses will not change.

(ii) No change Purchases and Closing Inventory will decrease by same amount and thus Operating

expenses will not change.

(iii) No change Purchases and Closing Inventory will decrease by same amount and thus Operating

expenses will not change.

(iv) No change No change in Operating Expenses as Machinery is an asset.

Cost of Revenue from Operations

(b) Inventory Turnover Ratio = = ... Times.

Average Inventory*

Opening Inventory + Closing Inventory

*Average Inventory =

2

23. CASH FLOW STATEMENT for the year ended 31st March, 2018

Particulars ` `

A. Cash Flow from Operating Activities

Net Profit before Tax and Extraordinary Items:

Closing Balance of Surplus, i.e., Balance in Statement of Profit and Loss 9,00,000

Less: Opening Balance of Surplus, i.e., Balance in Statement of Profit and Loss 5,00,000

4,00,000

Add: Provision for Tax (Current Year) 50,000

Interim Dividend 2,00,000

Dividend on Preference Shares* (12% of ` 10,00,000) 1,20,000

Net Profit before Tax 7,70,000

Adjustment for Non-Cash and Non-Operating Items:

Depreciation on Machinery 7,00,000

Interest on Debentures 1,00,000

Patents written off 40,000 8,40,000

16,10,000

Less: Gain (Profit) on Sale of Machinery (WN) 60,000

Operating Profit before Working Capital Changes 15,50,000

Add: Decrease in Current Assets and Increase in Current Liabilities:

Inventories 2,00,000

Trade Receivables 2,00,000

Trade Payables 9,50,000 13,50,000

Less: Decrease in Current Liabilities: 29,00,000

Outstanding Expenses 30,000

Net Cash Generated from Operating Activities 28,70,000

Less: Tax Paid 30,000

Cash Flow from Operating Activities 28,40,000