Page 334 - AAAXII

P. 334

Model Test Papers M.319

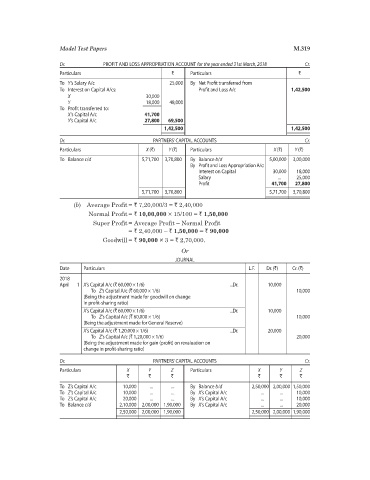

Dr. PROFIT AND LOSS APPROPRIATION ACCOUNT for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Y’s Salary A/c 25,000 By Net Profit transferred from

To Interest on Capital A/cs: Profit and Loss A/c 1,42,500

X 30,000

Y 18,000 48,000

To Profit transferred to:

X’s Capital A/c 41,700

Y’s Capital A/c 27,800 69,500

1,42,500 1,42,500

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X (`) Y (`) Particulars X (`) Y (`)

To Balance c/d 5,71,700 3,70,800 By Balance b/d 5,00,000 3,00,000

By Profit and Loss Appropriation A/c:

Interest on Capital 30,000 18,000

Salary ... 25,000

Profit 41,700 27,800

5,71,700 3,70,800 5,71,700 3,70,800

(b) Average Profit = ` 7,20,000/3 = ` 2,40,000

Normal Profit = ` 10,00,000 × 15/100 = ` 1,50,000

Super Profit = Average Profit – Normal Profit

= ` 2,40,000 – ` 1,50,000 = ` 90,000

Goodwill = ` 90,000 × 3 = ` 2,70,000.

Or

JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2018

April 1 X’s Capital A/c (` 60,000 × 1/6) ...Dr. 10,000

To Z’s Capital A/c (` 60,000 × 1/6) 10,000

(Being the adjustment made for goodwill on change

in profit-sharing ratio)

X’s Capital A/c (` 60,000 × 1/6) ...Dr. 10,000

To Z’s Capital A/c (` 60,000 × 1/6) 10,000

(Being the adjustment made for General Reserve)

X’s Capital A/c (` 1,20,000 × 1/6) ...Dr. 20,000

To Z’s Capital A/c (` 1,20,000 × 1/6) 20,000

(Being the adjustment made for gain (profit) on revaluation on

change in profit-sharing ratio)

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X Y Z Particulars X Y Z

` ` ` ` ` `

To Z’s Capital A/c 10,000 ... ... By Balance b/d 2,50,000 2,00,000 1,50,000

To Z’s Capital A/c 10,000 ... ... By X’s Capital A/c ... ... 10,000

To Z’s Capital A/c 20,000 ... ... By X’s Capital A/c ... ... 10,000

To Balance c/d 2,10,000 2,00,000 1,90,000 By X’s Capital A/c ... ... 20,000

2,50,000 2,00,000 1,90,000 2,50,000 2,00,000 1,90,000