Page 383 - AAAXII

P. 383

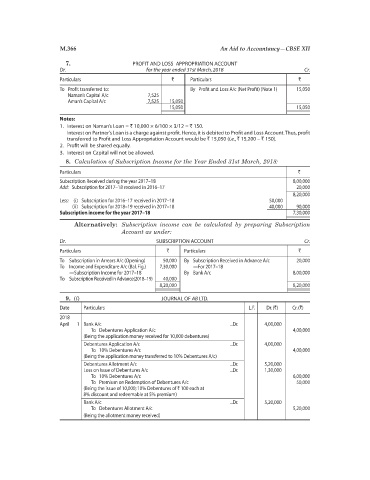

M.366 An Aid to Accountancy—CBSE XII

7. PROFIT AND LOSS APPROPRIATION ACCOUNT

Dr. for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Profit transferred to: By Profit and Loss A/c (Net Profit) (Note 1) 15,050

Naman’s Capital A/c 7,525

Aman’s Capital A/c 7,525 15,050

15,050 15,050

Notes:

1. Interest on Naman’s Loan = ` 10,000 × 6/100 × 3/12 = ` 150.

Interest on Partner’s Loan is a charge against profit. Hence, it is debited to Profit and Loss Account. Thus, profit

transferred to Profit and Loss Appropriation Account would be ` 15,050 (i.e., ` 15,200 – ` 150).

2. Profit will be shared equally.

3. Interest on Capital will not be allowed.

8. Calculation of Subscription Income for the Year Ended 31st March, 2018:

Particulars `

Subscription Received during the year 2017–18 8,00,000

Add: Subscription for 2017–18 received in 2016–17 20,000

8,20,000

Less: (i) Subscription for 2016–17 received in 2017–18 50,000

(ii) Subscription for 2018–19 received in 2017–18 40,000 90,000

Subscription income for the year 2017–18 7,30,000

Alternatively: Subscription income can be calculated by preparing Subscription

Account as under:

Dr. SUBSCRIPTION ACCOUNT Cr.

Particulars ` Particulars `

To Subscription in Arrears A/c (Opening) 50,000 By Subscription Received in Advance A/c 20,000

To Income and Expenditure A/c (Bal. Fig.) 7,30,000 —For 2017–18

—Subscription Income for 2017–18 By Bank A/c 8,00,000

To Subscription Received in Advance(2018–19) 40,000

8,20,000 8,20,000

9. (i) JOURNAL OF AB LTD.

Date Particulars L.F. Dr. (`) Cr. (`)

2018

April 1 Bank A/c ...Dr. 4,00,000

To Debentures Application A/c 4,00,000

(Being the application money received for 10,000 debentures)

Debentures Application A/c ...Dr. 4,00,000

To 10% Debentures A/c 4,00,000

(Being the application money transferred to 10% Debentures A/c)

Debentures Allotment A/c ...Dr. 5,20,000

Loss on Issue of Debentures A/c ...Dr. 1,30,000

To 10% Debentures A/c 6,00,000

To Premium on Redemption of Debentures A/c 50,000

(Being the issue of 10,000; 10% Debentures of ` 100 each at

8% discount and redeemable at 5% premium)

Bank A/c ...Dr. 5,20,000

To Debentures Allotment A/c 5,20,000

(Being the allotment money received)