Page 386 - AAAXII

P. 386

Model Test Papers M.369

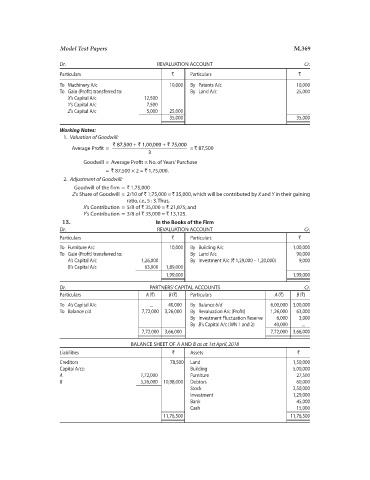

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Machinery A/c 10,000 By Patents A/c 10,000

To Gain (Profit) transferred to: By Land A/c 25,000

X’s Capital A/c 12,500

Y’s Capital A/c 7,500

Z’s Capital A/c 5,000 25,000

35,000 35,000

Working Notes:

1. Valuation of Goodwill:

` 87,500 + 1,00,000 + 75,000` `

Average Profit = = ` 87,500

3

Goodwill = Average Profit × No. of Years’ Purchase

= ` 87,500 × 2 = ` 1,75,000.

2. Adjustment of Goodwill:

Goodwill of the firm = ` 1,75,000

Z’s Share of Goodwill = 2/10 of ` 1,75,000 = ` 35,000, which will be contributed by X and Y in their gaining

ratio, i.e., 5 : 3. Thus,

X’s Contribution = 5/8 of ` 35,000 = ` 21,875; and

Y’s Contribution = 3/8 of ` 35,000 = ` 13,125.

13. In the Books of the Firm

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Furniture A/c 10,000 By Building A/c 1,00,000

To Gain (Profit) transferred to: By Land A/c 90,000

A’s Capital A/c 1,26,000 By Investment A/c (` 1,29,000 – 1,20,000) 9,000

B’s Capital A/c 63,000 1,89,000

1,99,000 1,99,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars A (`) B (`) Particulars A (`) B (`)

To A’s Capital A/c ... 40,000 By Balance b/d 6,00,000 3,00,000

To Balance c/d 7,72,000 3,26,000 By Revaluation A/c (Profit) 1,26,000 63,000

By Investment Fluctuation Reserve 6,000 3,000

By B’s Capital A/c (WN 1 and 2) 40,000 ...

7,72,000 3,66,000 7,72,000 3,66,000

BALANCE SHEET OF A AND B as at 1st April, 2018

Liabilities ` Assets `

Creditors 78,500 Land 1,50,000

Capital A/cs: Building 5,00,000

A 7,72,000 Furniture 27,500

B 3,26,000 10,98,000 Debtors 60,000

Stock 2,50,000

Investment 1,29,000

Bank 45,000

Cash 15,000

11,76,500 11,76,500