Page 70 - AAAXII

P. 70

Model Test Papers M.65

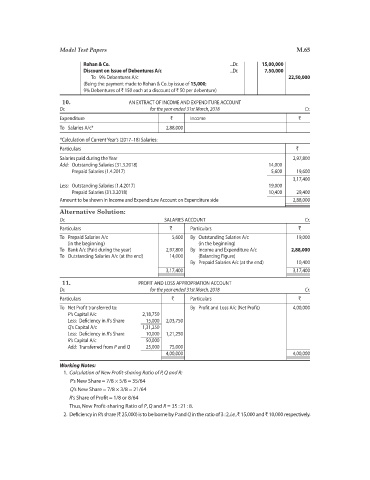

Rohan & Co. ...Dr. 15,00,000

Discount on Issue of Debentures A/c ...Dr. 7,50,000

To 9% Debentures A/c 22,50,000

(Being the payment made to Rohan & Co. by issue of 15,000;

9% Debentures of ` 150 each at a discount of ` 50 per debenture)

10. AN EXTRACT OF INCOME AND EXPENDITURE ACCOUNT

Dr. for the year ended 31st March, 2018 Cr.

Expenditure ` Income `

To Salaries A/c* 2,88,000

*Calculation of Current Year’s (2017–18) Salaries:

Particulars `

Salaries paid during the Year 2,97,800

Add: Outstanding Salaries (31.3.2018) 14,000

Prepaid Salaries (1.4.2017) 5,600 19,600

3,17,400

Less: Outstanding Salaries (1.4.2017) 19,000

Prepaid Salaries (31.3.2018) 10,400 29,400

Amount to be shown in Income and Expenditure Account on Expenditure side 2,88,000

Alternative Solution:

Dr. SALARIES ACCOUNT Cr.

Particulars ` Particulars `

To Prepaid Salaries A/c 5,600 By Outstanding Salaries A/c 19,000

(in the beginning) (in the beginning)

To Bank A/c (Paid during the year) 2,97,800 By Income and Expenditure A/c 2,88,000

To Outstanding Salaries A/c (at the end) 14,000 (Balancing Figure)

By Prepaid Salaries A/c (at the end) 10,400

3,17,400 3,17,400

11. PROFIT AND LOSS APPROPRIATION ACCOUNT

Dr. for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Net Profit transferred to: By Profit and Loss A/c (Net Profit) 4,00,000

P’s Capital A/c 2,18,750

Less: Deficiency in R’s Share 15,000 2,03,750

Q’s Capital A/c 1,31,250

Less: Deficiency in R’s Share 10,000 1,21,250

R’s Capital A/c 50,000

Add: Transferred from P and Q 25,000 75,000

4,00,000 4,00,000

Working Notes:

1. Calculation of New Profit-sharing Ratio of P, Q and R:

P’s New Share = 7/8 × 5/8 = 35/64

Q’s New Share = 7/8 × 3/8 = 21/64

R’s Share of Profit = 1/8 or 8/64

Thus, New Profit-sharing Ratio of P, Q and R = 35 : 21 : 8.

2. Deficiency in R’s share (` 25,000) is to be borne by P and Q in the ratio of 3 : 2, i.e., ` 15,000 and ` 10,000 respectively.