Page 73 - AAAXII

P. 73

M.68 An Aid to Accountancy—CBSE XII

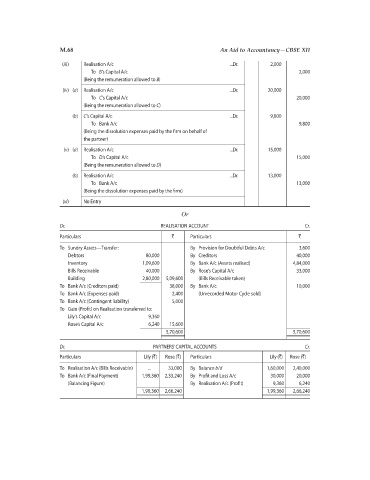

(iii) Realisation A/c ...Dr. 2,000

To B’s Capital A/c 2,000

(Being the remuneration allowed to B)

(iv) (a) Realisation A/c ...Dr. 20,000

To C’s Capital A/c 20,000

(Being the remuneration allowed to C)

(b) C’s Capital A/c ...Dr. 9,800

To Bank A/c 9,800

(Being the dissolution expenses paid by the firm on behalf of

the partner)

(v) (a) Realisation A/c ...Dr. 15,000

To D’s Capital A/c 15,000

(Being the remuneration allowed to D)

(b) Realisation A/c ...Dr. 13,000

To Bank A/c 13,000

(Being the dissolution expenses paid by the firm)

(vi) No Entry

Or

Dr. REALISATION ACCOUNT Cr.

Particulars ` Particulars `

To Sundry Assets—Transfer: By Provision for Doubtful Debts A/c 3,600

Debtors 80,000 By Creditors 40,000

Inventory 1,09,600 By Bank A/c (Assets realised) 4,84,000

Bills Receivable 40,000 By Rose’s Capital A/c 33,000

Building 2,80,000 5,09,600 (Bills Receivable taken)

To Bank A/c (Creditors paid) 38,000 By Bank A/c 10,000

To Bank A/c (Expenses paid) 2,400 (Unrecorded Motor Cycle sold)

To Bank A/c (Contingent liability) 5,000

To Gain (Profit) on Realisation transferred to:

Lily’s Capital A/c 9,360

Rose’s Capital A/c 6,240 15,600

5,70,600 5,70,600

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Lily (`) Rose (`) Particulars Lily (`) Rose (`)

To Realisation A/c (Bills Receivable) ... 33,000 By Balance b/d 1,60,000 2,40,000

To Bank A/c (Final Payment) 1,99,360 2,33,240 By Profit and Loss A/c 30,000 20,000

(Balancing Figure) By Realisation A/c (Profit) 9,360 6,240

1,99,360 2,66,240 1,99,360 2,66,240