Page 96 - AAAXII

P. 96

M.90 An Aid to Accountancy—CBSE XII

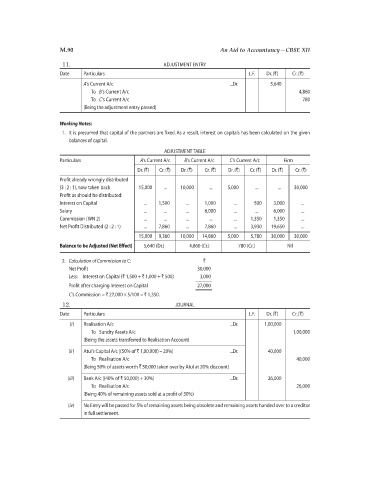

11. ADJUSTMENT ENTRY

Date Particulars L.F. Dr. (`) Cr. (`)

A’s Current A/c ...Dr. 5,640

To B’s Current A/c 4,860

To C’s Current A/c 780

(Being the adjustment entry passed)

Working Notes:

1. It is presumed that capital of the partners are fixed. As a result, interest on capitals has been calculated on the given

balances of capital.

ADJUSTMENT TABLE

Particulars A’s Current A/c B’s Current A/c C’s Current A/c Firm

Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`) Dr. (`) Cr. (`)

Profit already wrongly distributed

(3 : 2 : 1), now taken back 15,000 ... 10,000 ... 5,000 ... ... 30,000

Profit as should be distributed:

Interest on Capital ... 1,500 ... 1,000 ... 500 3,000 ...

Salary ... ... ... 6,000 ... ... 6,000 ...

Commission (WN 2) ... ... ... ... ... 1,350 1,350 ...

Net Profit Distributed (2 : 2 : 1) ... 7,860 ... 7,860 ... 3,930 19,650 ...

15,000 9,360 10,000 14,860 5,000 5,780 30,000 30,000

Balance to be Adjusted (Net Effect) 5,640 (Dr.) 4,860 (Cr.) 780 (Cr.) Nil

2. Calculation of Commission to C: `

Net Profit 30,000

Less: Interest on Capital (` 1,500 + ` 1,000 + ` 500) 3,000

Profit after charging Interest on Capital 27,000

C’s Commission = ` 27,000 × 5/100 = ` 1,350.

12. JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

(i) Realisation A/c ...Dr. 1,00,000

To Sundry Assets A/c 1,00,000

(Being the assets transferred to Realisation Account)

(ii) Atul’s Capital A/c [(50% of ` 1,00,000) – 20%] ...Dr. 40,000

To Realisation A/c 40,000

(Being 50% of assets worth ` 50,000 taken over by Atul at 20% discount)

(iii) Bank A/c [(40% of ` 50,000) + 30%] ...Dr. 26,000

To Realisation A/c 26,000

(Being 40% of remaining assets sold at a profit of 30%)

(iv) No Entry will be passed for 5% of remaining assets being obsolete and remaining assets handed over to a creditor

in full settlement.