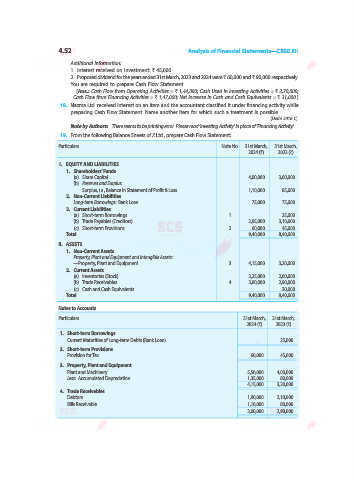

Page 134 - afs12

P. 134

5.34 Analysis of Financial Statements—CBSE XII

Notes to Accounts

Particulars 31st March, 31st March,

2025 (`) 2024 (`)

1. Trade Payables

Creditors 55,000 50,000

Bills Payable 20,000 50,000

75,000 1,00,000

2. Property, Plant and Equipment

Building 2,50,000 4,00,000

Plant and Machinery 2,70,000 3,00,000

5,20,000 7,00,000

3. Current Investments

Investment in Securities (Other than Marketable Securities) 90,000 ...

Additional Information:

1. ` 50,000 as Interim Dividend was paid during the year.

2. Building is sold at book value.

Solution: CASH FLOW STATEMENT for the year ended 31st March, 2025

Particulars `

(A) Cash Flow from Operating Activities

Net Profit before Tax and Extraordinary Items (WN) 2,65,000

Add: Non-Cash Items and Non-operating Items:

Goodwill amortised (` 1,00,000 – ` 50,000) 50,000

Depreciation on Plant and Machinery (` 3,00,000 – ` 2,70,000) 30,000

Interest on Debentures 6,000

Operating Profit before Working Capital Changes 3,51,000

Add: Decrease in Current Assets and Increase in Current Liabilities:

Creditors (Trade Payables) 5,000

Inventories 10,000

3,66,000

Less: Increase in Current Assets and Decrease in Current Liabilities:

Trade Receivables 40,000

Bills Payable (Trade Payables) 30,000 70,000

Cash Generated from Operating Activities 2,96,000

Less: Tax Paid 50,000

Cash Flow from Operating Activities 2,46,000

(B) Cash Flow from Investing Activities

Proceeds from Sale of Building 1,50,000

Purchase of Non-Current Investments (2,70,000)

Purchase of Securities (90,000)

Cash Used in Investing Activities (2,10,000)

(C) Cash Flow from Financing Activities

Proceeds from Issue of Shares 3,00,000

Payment of Interest on Debentures (6,000)

Payment of Interim Dividend (50,000)

Proceeds from raising of Bank Loan 50,000

Cash Flow from Financing Activities 2,94,000

(D) Net Increase In Cash and Cash Equivalents (A + B + C) 3,30,000

Add: Cash and Cash Equivalents in the beginning of the year 50,000

(E) Cash and Cash Equivalents at the end of the year 3,80,000