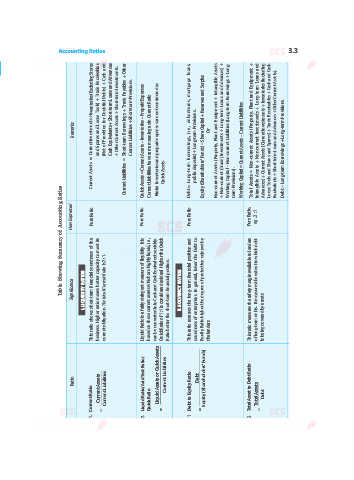

Page 31 - afs12

P. 31

3.4 Analysis of Financial Statements—CBSE XII

FORMAT OF COMPARATIVE STATEMENT OF PROFIT & LOSS

COMPARATIVE STATEMENT OF PROFIT & LOSS

for the years ended...

Particulars Note Previous Current Absolute Percentage

No. Year Year Change (Increase Change (Increase

` ` or Decrease) (`) or Decrease) (%)

(C = B – A) C

(A) (B) D 100

A

I. Revenue from Operations ... ... ... ...

II. Other Income ... ... ... ...

III. Total Revenue (I + II) ... ... ... ...

IV. Expenses

(a) Cost of Materials Consumed ... ... ... ...

(b) Purchases of Stock-in-Trade ... ... ... ...

(c) Changes in Inventories of Finished Goods,

Work-in-Progress and Stock-in-Trade ... ... ... ...

(d) Employees Benefit Expenses ... ... ... ...

(e) Finance Costs ... ... ... ...

(f) Depreciation and Amortisation Expenses ... ... ... ...

(g) Other Expenses ... ... ... ...

Total Expenses ... ... ... ...

V. Profit before Tax (III – IV) ... ... ... ...

Less: Income Tax ... ... ... ...

VI. Profit after Tax ... ... ... ...

Note: If current year’s figure has decreased, show the Absolute change and Percentage change in brackets so

as to reflect negative item.

FORMAT OF COMMON-SIZE STATEMENT OF PROFIT & LOSS (INCOME STATEMENT)

COMMON-SIZE STATEMENT OF PROFIT & LOSS

for the years ended...

Particulars Note Absolute Amounts Percentage of Revenue from

No. Operations (Net Sales)

Previous Year Current Year Previous Year Current Year

` ` % %

I. Revenue from Operations (Net Sales) ... ... 100 100

II. Other Income ... ... ... ...

III. Total Revenue (I + II) ... ... ... ...

IV. Expenses

(a) Cost of Materials Consumed ... ... ... ...

(b) Purchases of Stock-in-Trade ... ... ... ...

(c) Changes in Inventories of Finished Goods,

Work-in-Progress and Stock-in-Trade ... ... ... ...

(d) Employees Benefit Expenses ... ... ... ...

(e) Finance Costs ... ... ... ...

(f) Depreciation and Amortisation Expenses ... ... ... ...

(g) Other Expenses ... ... ... ...

Total Expenses ... ... ... ...

V. Profit before Tax (III – IV) ... ... ... ...

VI. Less: Income Tax ... ... ... ...

VII. Profit after Tax ... ... ... ...