Page 32 - afs12

P. 32

Comparative Statements and Common-Size Statements 3.5

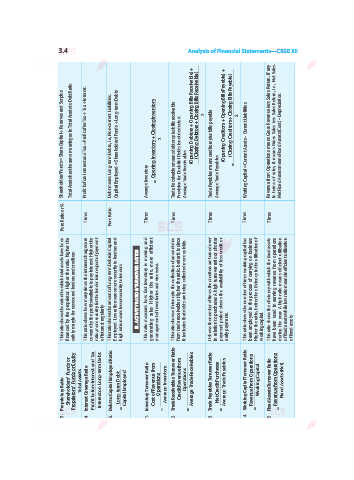

FORMAT OF COMMON-SIZE BALANCE SHEET

COMMON-SIZE BALANCE SHEET

as at...

Particulars Note Absolute Amounts Percentage of

No. Balance Sheet Total

Figures as at the end Figures as at the end Previous Year Current Year

of Previous Year (`) of Current Year (`) % %

I. EQUITY AND LIABILITIES

1. Shareholders’ Funds

(a) Share Capital:

(i) Equity Share Capital ... ... ... ...

(ii) Preference Share Capital ... ... ... ...

(b) Reserves and Surplus ... ... ... ...

2. Non-Current Liabilities

(a) Long-term Borrowings ... ... ... ...

(b) Long-term Provisions ... ... ... ...

3. Current Liabilities

(a) Short-term Borrowings ... ... ... ...

(b) Trade Payables ... ... ... ...

(c) Other Current Liabilities ... ... ... ...

(d) Short-term Provisions ... ... ... ...

Total ... ... 100 100

II. ASSETS

1. Non-Current Assets

(a) Property, Plant and Equipment

and Intangible Assets:

(i) Property, Plant and Equipment ... ... ... ...

(ii) Intangible Assets ... ... ... ...

(b) Non-current Investments ... ... ... ...

(c) Long-term Loans and Advances ... ... ... ...

2. Current Assets

(a) Current Investments ... ... ... ...

(b) Inventories ... ... ... ...

(c) Trade Receivables ... ... ... ...

(d) Cash and Cash Equivalents ... ... ... ...

(e) Short-term Loans and Advances ... ... ... ...

(f) Other Current Assets ... ... ... ...

Total ... ... 100 100

Note: It does not include line items of Balance Sheet, accounting treatment of which are not to be evaluated.