Page 94 - DEBK11

P. 94

CHAPTER Trial Balance

CHAPTER

14

MEANING OF KEY TERMS USED IN THE CHAPTER

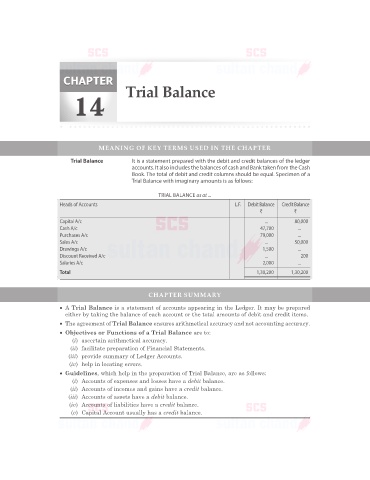

Trial Balance It is a statement prepared with the debit and credit balances of the ledger

accounts. It also includes the balances of cash and Bank taken from the Cash

Book. The total of debit and credit columns should be equal. Specimen of a

Trial Balance with imaginary amounts is as follows:

TRIAL BALANCE as at ...

Heads of Accounts L.F. Debit Balance Credit Balance

` `

Capital A/c ... 80,000

Cash A/c 47,700 ...

Purchases A/c 79,000 ...

Sales A/c ... 50,000

Drawings A/c 1,500 ...

Discount Received A/c ... 200

Salaries A/c 2,000 ...

Total 1,30,200 1,30,200

CHAPTER SUMMARY

• A Trial Balance is a statement of accounts appearing in the Ledger. It may be prepared

either by taking the balance of each account or the total amounts of debit and credit items.

• The agreement of Trial Balance ensures arithmetical accuracy and not accounting accuracy.

• Objectives or Functions of a Trial Balance are to:

(i) ascertain arithmetical accuracy.

(ii) facilitate preparation of Financial Statements.

(iii) provide summary of Ledger Accounts.

(iv) help in locating errors.

• Guidelines, which help in the preparation of Trial Balance, are as follows:

(i) Accounts of expenses and losses have a debit balance.

(ii) Accounts of incomes and gains have a credit balance.

(iii) Accounts of assets have a debit balance.

(iv) Accounts of liabilities have a credit balance.

(v) Capital Account usually has a credit balance.