Page 99 - DEBK11

P. 99

14.6 Double Entry Book Keeping—CBSE XI

Working Notes:

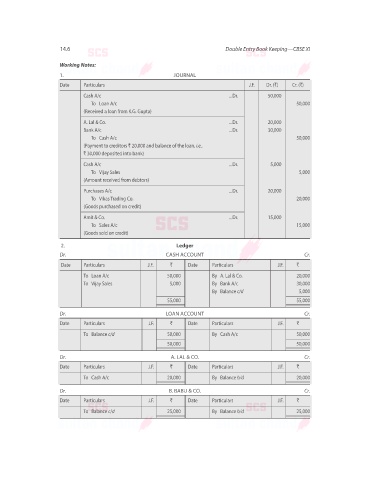

1. JOURNAL

Date Particulars J.F. Dr. (`) Cr. (`)

Cash A/c ...Dr. 50,000

To Loan A/c 50,000

(Received a loan from K.G. Gupta)

A. Lal & Co. ...Dr. 20,000

Bank A/c ...Dr. 30,000

To Cash A/c 50,000

(Payment to creditors ` 20,000 and balance of the loan, i.e.,

` 30,000 deposited into bank)

Cash A/c ...Dr. 5,000

To Vijay Sales 5,000

(Amount received from debtors)

Purchases A/c ...Dr. 20,000

To Vikas Trading Co. 20,000

(Goods purchased on credit)

Amit & Co. ...Dr. 15,000

To Sales A/c 15,000

(Goods sold on credit)

2. Ledger

Dr. CASH ACCOUNT Cr.

Date Particulars J.F. ` Date Particulars J.F. `

To Loan A/c 50,000 By A. Lal & Co. 20,000

To Vijay Sales 5,000 By Bank A/c 30,000

By Balance c/d 5,000

55,000 55,000

Dr. LOAN ACCOUNT Cr.

Date Particulars J.F. ` Date Particulars J.F. `

To Balance c/d 50,000 By Cash A/c 50,000

50,000 50,000

Dr. A. LAL & CO. Cr.

Date Particulars J.F. ` Date Particulars J.F. `

To Cash A/c 20,000 By Balance b/d 20,000

Dr. B. BABU & CO. Cr.

Date Particulars J.F. ` Date Particulars J.F. `

To Balance c/d 25,000 By Balance b/d 25,000