Page 102 - ISCDEBK-XI

P. 102

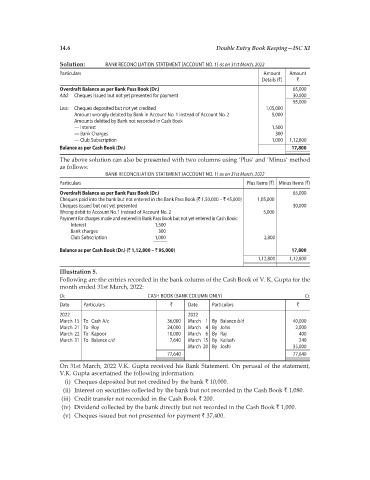

14.6 Double Entry Book Keeping—ISC XI

Solution: BANK RECONCILIATION STATEMENT (ACCOUNT NO. 1) as on 31st March, 2022

Particulars Amount Amount

Details (`) `

Overdraft Balance as per Bank Pass Book (Dr.) 65,000

Add: Cheques issued but not yet presented for payment 30,000

95,000

Less: Cheques deposited but not yet credited 1,05,000

Amount wrongly debited by Bank in Account No. 1 instead of Account No. 2 5,000

Amounts debited by Bank not recorded in Cash Book

— Interest 1,500

— Bank Charges 300

— Club Subscription 1,000 1,12,800

Balance as per Cash Book (Dr.) 17,800

The above solution can also be presented with two columns using ‘Plus’ and ’Minus’ method

as follows:

BANK RECONCILIATION STATEMENT (ACCOUNT NO. 1) as on 31st March, 2022

Particulars Plus Items (`) Minus Items (`)

Overdraft Balance as per Bank Pass Book (Dr.) 65,000

Cheques paid into the bank but not entered in the Bank Pass Book (` 1,50,000 – ` 45,000) 1,05,000

Cheques issued but not yet presented 30,000

Wrong debit to Account No. 1 instead of Account No. 2 5,000

Payment for charges made and entered in Bank Pass Book but not yet entered in Cash Book:

Interest 1,500

Bank charges 300

Club Subscription 1,000 2,800

Balance as per Cash Book (Dr.) (` 1,12,800 – ` 95,000) 17,800

1,12,800 1,12,800

Illustration 5.

Following are the entries recorded in the bank column of the Cash Book of V. K. Gupta for the

month ended 31st March, 2022:

Dr. CASH BOOK (BANK COLUMN ONLY) Cr.

Date Particulars ` Date Particulars `

2022 2022

March 15 To Cash A/c 36,000 March 1 By Balance b/d 40,000

March 21 To Roy 24,000 March 4 By John 2,000

March 22 To Kapoor 10,000 March 6 By Raj 400

March 31 To Balance c/d 7,640 March 15 By Kailash 240

March 20 By Joshi 35,000

77,640 77,640

On 31st March, 2022 V.K. Gupta received his Bank Statement. On perusal of the statement,

V.K. Gupta ascertained the following information:

(i) Cheques deposited but not credited by the bank ` 10,000.

(ii) Interest on securities collected by the bank but not recorded in the Cash Book ` 1,080.

(iii) Credit transfer not recorded in the Cash Book ` 200.

(iv) Dividend collected by the bank directly but not recorded in the Cash Book ` 1,000.

(v) Cheques issued but not presented for payment ` 37,400.