Page 258 - MA-12

P. 258

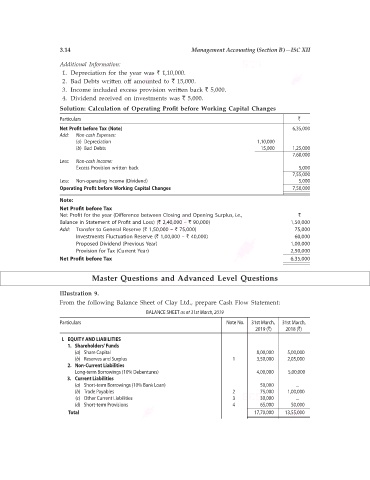

3.14 Management Accounting (Section B)—ISC XII

Additional Information:

1. Depreciation for the year was ` 1,10,000.

2. Bad Debts written off amounted to ` 15,000.

3. Income included excess provision written back ` 5,000.

4. Dividend received on investments was ` 5,000.

Solution: Calculation of Operating Profit before Working Capital Changes

Particulars `

Net Profit before Tax (Note) 6,35,000

Add: Non-cash Expenses:

(a) Depreciation 1,10,000

(b) Bad Debts 15,000 1,25,000

7,60,000

Less: Non-cash Income:

Excess Provision written back 5,000

7,55,000

Less: Non-operating Income (Dividend) 5,000

Operating Profit before Working Capital Changes 7,50,000

Note:

Net Profit before Tax

Net Profit for the year (Difference between Closing and Opening Surplus, i.e., `

Balance in Statement of Profit and Loss) (` 2,40,000 – ` 90,000) 1,50,000

Add: Transfer to General Reserve (` 1,50,000 – ` 75,000) 75,000

Investments Fluctuation Reserve (` 1,00,000 – ` 40,000) 60,000

Proposed Dividend (Previous Year) 1,00,000

Provision for Tax (Current Year) 2,50,000

Net Profit before Tax 6,35,000

Master Questions and Advanced Level Questions

Illustration 9.

From the following Balance Sheet of Clay Ltd., prepare Cash Flow Statement:

BALANCE SHEET as at 31st March, 2019

Particulars Note No. 31st March, 31st March,

2019 (`) 2018 (`)

I. EQUITY AND LIABILITIES

1. Shareholders’ Funds

(a) Share Capital 8,00,000 5,00,000

(b) Reserves and Surplus 1 3,50,000 2,05,000

2. Non-Current Liabilities

Long-term Borrowings (10% Debentures) 4,00,000 5,00,000

3. Current Liabilities

(a) Short-term Borrowings (10% Bank Loan) 50,000 ...

(b) Trade Payables 2 75,000 1,00,000

(c) Other Current Liabilities 3 30,000 ...

(d) Short-term Provisions 4 65,000 50,000

Total 17,70,000 13,55,000