Page 110 - DEBKVOL-1

P. 110

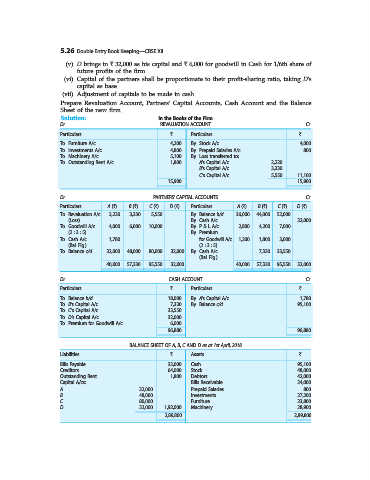

5.26 Double Entry Book Keeping—CBSE XII

(v) D brings in ` 32,000 as his capital and ` 6,000 for goodwill in Cash for 1/6th share of

future profits of the firm.

(vi) Capital of the partners shall be proportionate to their profit-sharing ratio, taking D’s

capital as base.

(vii) Adjustment of capitals to be made in cash.

Prepare Revaluation Account, Partners’ Capital Accounts, Cash Account and the Balance

Sheet of the new firm.

Solution: In the Books of the Firm

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Furniture A/c 4,200 By Stock A/c 4,000

To Investments A/c 4,800 By Prepaid Salaries A/c 800

To Machinery A/c 5,100 By Loss transferred to:

To Outstanding Rent A/c 1,800 A’s Capital A/c 2,220

B’s Capital A/c 3,330

C’s Capital A/c 5,550 11,100

15,900 15,900

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars A (`) B (`) C (`) D (`) Particulars A (`) B (`) C (`) D (`)

To Revaluation A/c 2,220 3,330 5,550 ... By Balance b/d 36,000 44,000 52,000 ...

(Loss) By Cash A/c ... ... ... 32,000

To Goodwill A/c 4,000 6,000 10,000 ... By P & L A/c 2,800 4,200 7,000 ...

(2 : 3 : 5) By Premium

To Cash A/c 1,780 ... ... ... for Goodwill A/c 1,200 1,800 3,000 ...

(Bal. Fig.) (2 : 3 : 5)

To Balance c/d 32,000 48,000 80,000 32,000 By Cash A/c ... 7,330 33,550 ...

(Bal. Fig.)

40,000 57,330 95,550 32,000 40,000 57,330 95,550 32,000

Dr. CASH ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 18,000 By A’s Capital A/c 1,780

To B’s Capital A/c 7,330 By Balance c/d 95,100

To C’s Capital A/c 33,550

To D’s Capital A/c 32,000

To Premium for Goodwill A/c 6,000

96,880 96,880

BALANCE SHEET OF A, B, C AND D as at 1st April, 2018

Liabilities ` Assets `

Bills Payable 32,000 Cash 95,100

Creditors 64,000 Stock 48,000

Outstanding Rent 1,800 Debtors 42,000

Capital A/cs: Bills Receivable 24,000

A 32,000 Prepaid Salaries 800

B 48,000 Investments 27,200

C 80,000 Furniture 23,800

D 32,000 1,92,000 Machinery 28,900

2,89,800 2,89,800