Page 108 - DEBKVOL-1

P. 108

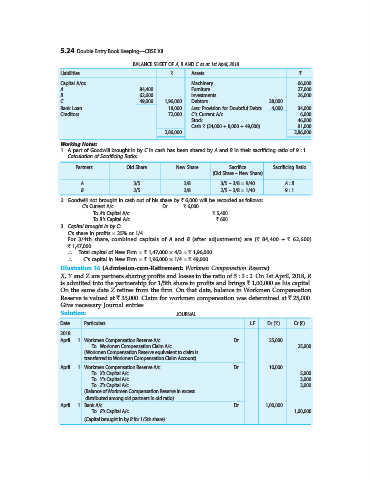

5.24 Double Entry Book Keeping—CBSE XII

BALANCE SHEET OF A, B AND C as at 1st April, 2018

Liabilities ` Assets `

Capital A/cs: Machinery 66,000

A 84,400 Furniture 27,000

B 62,600 Investments 26,000

C 49,000 1,96,000 Debtors 38,000

Bank Loan 18,000 Less: Provision for Doubtful Debts 4,000 34,000

Creditors 72,000 C’s Current A/c 6,000

Stock 46,000

Cash ` (24,000 + 8,000 + 49,000) 81,000

2,86,000 2,86,000

Working Notes:

1. A part of Goodwill brought in by C in cash has been shared by A and B in their sacrificing ratio of 9 : 1.

Calculation of Sacrificing Ratio:

Partners Old Share New Share Sacrifice Sacrificing Ratio

(Old Share – New Share)

A 3/5 3/8 3/5 – 3/8 = 9/40 A : B

B 2/5 3/8 2/5 – 3/8 = 1/40 9 : 1

2. Goodwill not brought in cash out of his share by ` 6,000 will be recorded as follows:

C’s Current A/c ...Dr. ` 6,000

To A’s Capital A/c ` 5,400

To B’s Capital A/c ` 600

3. Capital brought in by C:

C’s share in profits = 25% or 1/4

For 3/4th share, combined capitals of A and B (after adjustments) are (` 84,400 + ` 62,600)

` 1,47,000.

∴ Total capital of New Firm = ` 1,47,000 × 4/3 = ` 1,96,000.

∴ C’s capital in New Firm = ` 1,96,000 × 1/4 = ` 49,000.

Illustration 16 (Admission-cum-Retirement: Workmen Compensation Reserve).

X, Y and Z are partners sharing profits and losses in the ratio of 5 : 3 : 2. On 1st April, 2018, R

is admitted into the partnership for 1/5th share in profits and brings ` 1,00,000 as his capital.

On the same date Z retires from the firm. On that date, balance in Workmen Compensation

Reserve is valued at ` 35,000. Claim for workmen compensation was determined at ` 25,000.

Give necessary Journal entries.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2018

April 1 Workmen Compensation Reserve A/c ...Dr. 25,000

To Workmen Compensation Claim A/c 25,000

(Workmen Compensation Reserve equivalent to claim is

transferred to Workmen Compensation Claim Account)

April 1 Workmen Compensation Reserve A/c ...Dr. 10,000

To X’s Capital A/c 5,000

To Y’s Capital A/c 3,000

To Z’s Capital A/c 2,000

(Balance of Workmen Compensation Reserve in excess

distributed among old partners in old ratio)

April 1 Bank A/c ...Dr. 1,00,000

To R’s Capital A/c 1,00,000

(Capital brought in by R for 1/5th share)