Page 213 - DEBKVOL-1

P. 213

8.38 Double Entry Book Keeping—CBSE XII

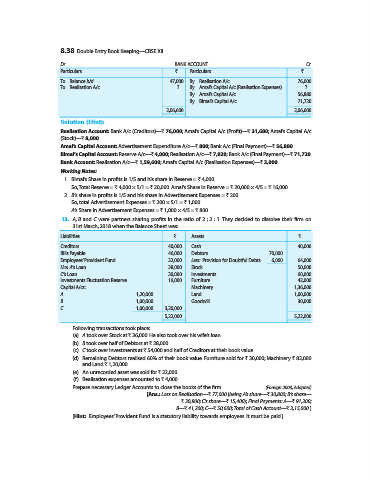

Dr. BANK ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 47,000 By Realisation A/c 76,000

To Realisation A/c ? By Amal’s Capital A/c (Realisation Expenses) ?

By Amal’s Capital A/c 56,880

By Bimal’s Capital A/c 71,720

2,06,600 2,06,600

Solution (Hint):

Realisation Account: Bank A/c (Creditors)—` 76,000; Amal’s Capital A/c (Profit)—` 31,680; Amal’s Capital A/c

(Stock)—` 8,000.

Amal’s Capital Account: Advertisement Expenditure A/c—` 800; Bank A/c (Final Payment)—` 56,880.

Bimal’s Capital Account: Reserve A/c—` 4,000; Realisation A/c—` 7,920; Bank A/c (Final Payment)—` 71,720.

Bank Account: Realisation A/c—` 1,59,600; Amal’s Capital A/c (Realisation Expenses)—` 2,000.

Working Notes:

1. Bimal’s Share in profits is 1/5 and his share in Reserve = ` 4,000.

So, Total Reserve = ` 4,000 × 5/1 = ` 20,000. Amal’s Share in Reserve = ` 20,000 × 4/5 = ` 16,000.

2. B’s share in profits is 1/5 and his share in Advertisement Expenses = ` 200.

So, total Advertisement Expenses = ` 200 × 5/1 = ` 1,000.

A’s Share in Advertisement Expenses = ` 1,000 × 4/5 = ` 800.

13. A, B and C were partners sharing profits in the ratio of 2 : 2 : 1. They decided to dissolve their firm on

31st March, 2018 when the Balance Sheet was:

Liabilities ` Assets `

Creditors 40,000 Cash 40,000

Bills Payable 46,000 Debtors 70,000

Employees’ Provident Fund 32,000 Less: Provision for Doubtful Debts 6,000 64,000

Mrs. A’s Loan 38,000 Stock 50,000

C’s Loan 30,000 Investments 60,000

Investments Fluctuation Reserve 16,000 Furniture 42,000

Capital A/cs: Machinery 1,36,000

A 1,20,000 Land 1,00,000

B 1,00,000 Goodwill 30,000

C 1,00,000 3,20,000

5,22,000 5,22,000

Following transactions took place:

(a) A took over Stock at ` 36,000. He also took over his wife’s loan.

(b) B took over half of Debtors at ` 28,000.

(c) C took over Investments at ` 54,000 and half of Creditors at their book value.

(d) Remaining Debtors realised 60% of their book value. Furniture sold for ` 30,000; Machinery ` 82,000

and Land ` 1,20,000.

(e) An unrecorded asset was sold for ` 22,000.

(f) Realisation expenses amounted to ` 4,000.

Prepare necessary Ledger Accounts to close the books of the firm. (Foreign 2003, Adapted)

[Ans.: Loss on Realisation—` 77,000 (being A’s share—` 30,800; B’s share—

` 30,800; C’s share—` 15,400); Final Payments: A—` 91,200;

B—` 41,200; C—` 50,600; Total of Cash Account—` 3,15,000.]

[Hint: Employees’ Provident Fund is a statutory liability towards employees. It must be paid.]