Page 210 - DEBKVOL-1

P. 210

Chapter 8 Dissolution of a Partnership Firm 8.35

.

(b) Amar also took over Land at book value and Plant at ` 12,000.

(c) Loose Tools, Stock and Sundry Debtors realised ` 2,000; ` 15,000 and ` 22,000 respectively.

(d) Sundry Creditors were paid off at a discount of 10%.

(e) The expenses of realisation were ` 1,500.

(f) A contingent liability of ` 1,000 which occurred during the period was duly paid-off.

[Ans.: Loss on Realisation—` 7,600; Cash paid to Akbar—` 18,960; Antony—` 14,480;

Cash brought in by Amar—` 40; Total of Bank A/c—` 44,040.]

Note: Amar’s Capital Account shows a debit balance of ` 7,040 (after all adjustments) so we have transferred

his Loan Account to his Capital Account for final settlement.

6. Cloud, Storm and Rain were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. Due to

difference in opinion, they decided to dissolve the partnership with effect from 1st April, 2018 on which

date the firm’s position was as under:

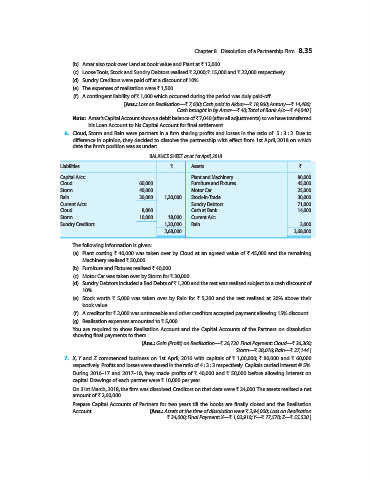

BALANCE SHEET as at 1st April, 2018

Liabilities ` Assets `

Capital A/cs: Plant and Machinery 80,000

Cloud 60,000 Furniture and Fixtures 45,000

Storm 40,000 Motor Car 25,000

Rain 30,000 1,30,000 Stock-in-Trade 30,000

Current A/cs: Sundry Debtors 71,000

Cloud 8,000 Cash at Bank 14,000

Storm 10,000 18,000 Current A/c:

Sundry Creditors 1,20,000 Rain 3,000

2,68,000 2,68,000

The following information is given:

(a) Plant costing ` 40,000 was taken over by Cloud at an agreed value of ` 45,000 and the remaining

Machinery realised ` 50,000.

(b) Furniture and Fixtures realised ` 40,000.

(c) Motor Car was taken over by Storm for ` 30,000.

(d) Sundry Debtors included a Bad Debts of ` 1,200 and the rest was realised subject to a cash discount of

10%.

(e) Stock worth ` 5,000 was taken over by Rain for ` 5,200 and the rest realised at 20% above their

book value.

(f) A creditor for ` 2,000 was untraceable and other creditors accepted payment allowing 15% discount.

(g) Realisation expenses amounted to ` 5,000.

You are required to show Realisation Account and the Capital Accounts of the Partners on dissolution

showing final payments to them.

[Ans.: Gain (Profit) on Realisation—` 26,720. Final Payment: Cloud—` 36,360;

Storm—` 28,016; Rain—` 27,144.]

7. X, Y and Z commenced business on 1st April, 2016 with capitals of ` 1,00,000; ` 80,000 and ` 60,000

respectively. Profits and losses were shared in the ratio of 4 : 3 : 3 respectively. Capitals carried interest @ 5%.

During 2016–17 and 2017–18, they made profits of ` 40,000 and ` 50,000 before allowing interest on

capital. Drawings of each partner were ` 10,000 per year.

On 31st March, 2018, the firm was dissolved. Creditors on that date were ` 24,000. The assets realised a net

amount of ` 2,60,000.

Prepare Capital Accounts of Partners for two years till the books are finally closed and the Realisation

Account. [Ans.: Assets at the time of dissolution were ` 2,94,000; Loss on Realisation

` 34,000; Final Payment: X—` 1,02,910; Y—` 77,570; Z—` 55,520.]