Page 211 - DEBKVOL-1

P. 211

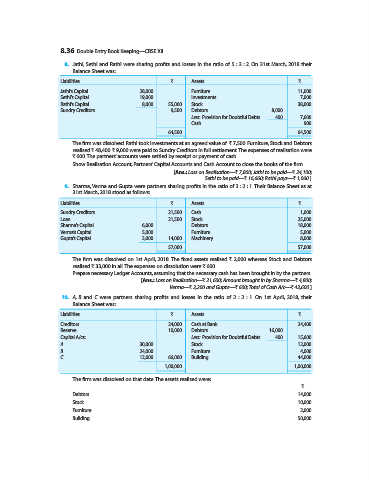

8.36 Double Entry Book Keeping—CBSE XII

8. Jathi, Sethi and Rathi were sharing profits and losses in the ratio of 5 : 3 : 2. On 31st March, 2018 their

Balance Sheet was:

Liabilities ` Assets `

Jathi’s Capital 28,000 Furniture 11,000

Sethi’s Capital 19,000 Investments 7,000

Rathi’s Capital 8,000 55,000 Stock 38,000

Sundry Creditors 9,500 Debtors 8,000

Less: Provision for Doubtful Debts 400 7,600

Cash 900

64,500 64,500

The firm was dissolved. Rathi took Investments at an agreed value of ` 7,500. Furniture, Stock and Debtors

realised ` 48,400. ` 9,000 were paid to Sundry Creditors in full settlement. The expenses of realisation were

` 600. The partners’ accounts were settled by receipt or payment of cash.

Show Realisation Account, Partners’ Capital Accounts and Cash Account to close the books of the firm.

[Ans.: Loss on Realisation—` 7,800; Jathi to be paid—` 24,100;

Sethi to be paid—` 16,660; Rathi pays—` 1,060.]

9. Sharma, Verma and Gupta were partners sharing profits in the ratio of 3 : 2 : 1. Their Balance Sheet as at

31st March, 2018 stood as follows:

Liabilities ` Assets `

Sundry Creditors 21,500 Cash 1,000

Loan 21,500 Stock 25,000

Sharma’s Capital 6,000 Debtors 18,000

Verma’s Capital 5,000 Furniture 5,000

Gupta’s Capital 3,000 14,000 Machinery 8,000

57,000 57,000

The firm was dissolved on 1st April, 2018. The fixed assets realised ` 2,000 whereas Stock and Debtors

realised ` 33,000 in all. The expenses on dissolution were ` 600.

Prepare necessary Ledger Accounts, assuming that the necessary cash has been brought in by the partners.

[Ans.: Loss on Realisation—` 21,600; Amount brought in by Sharma—` 4,800;

Verma—` 2,200 and Gupta—` 600; Total of Cash A/c—` 43,600.]

10. A, B and C were partners sharing profits and losses in the ratio of 2 : 2 : 1. On 1st April, 2018, their

Balance Sheet was:

Liabilities ` Assets `

Creditors 24,000 Cash at Bank 24,400

Reserve 10,000 Debtors 16,000

Capital A/cs: Less: Provision for Doubtful Debts 400 15,600

A 30,000 Stock 12,000

B 24,000 Furniture 4,000

C 12,000 66,000 Building 44,000

1,00,000 1,00,000

The firm was dissolved on that date. The assets realised were:

`

Debtors 14,000

Stock 10,000

Furniture 2,000

Building 50,000