Page 40 - DEBKVOL-1

P. 40

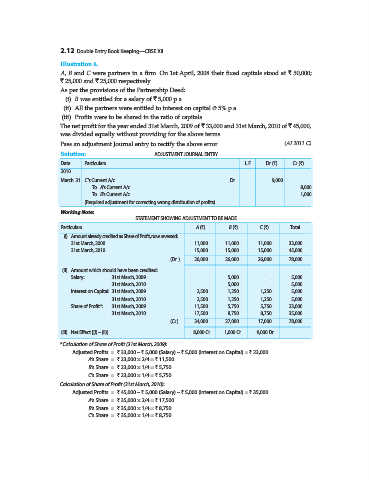

2.12 Double Entry Book Keeping—CBSE XII

Illustration 6.

A, B and C were partners in a firm. On 1st April, 2008 their fixed capitals stood at ` 50,000;

` 25,000 and ` 25,000 respectively.

As per the provisions of the Partnership Deed:

(i) B was entitled for a salary of ` 5,000 p.a.

(ii) All the partners were entitled to interest on capital @ 5% p.a.

(iii) Profits were to be shared in the ratio of capitals.

The net profit for the year ended 31st March, 2009 of ` 33,000 and 31st March, 2010 of ` 45,000,

was divided equally without providing for the above terms.

Pass an adjustment Journal entry to rectify the above error. (AI 2011 C)

Solution: ADJUSTMENT JOURNAL ENTRY

Date Particulars L.F. Dr. (`) Cr. (`)

2010

March 31 C’s Current A/c ...Dr. 9,000

To A’s Current A/c 8,000

To B’s Current A/c 1,000

(Required adjustment for correcting wrong distribution of profits)

Working Note:

STATEMENT SHOWING ADJUSTMENT TO BE MADE

Particulars A (`) B (`) C (`) Total

(i) Amount already credited as Share of Profit, now reversed:

31st March, 2009 11,000 11,000 11,000 33,000

31st March, 2010 15,000 15,000 15,000 45,000

(Dr..) 26,000 26,000 26,000 78,000

(ii) Amount which should have been credited:

Salary: 31st March, 2009 ... 5,000 ... 5,000

31st March, 2010 ... 5,000 ... 5,000

Interest on Capital: 31st March, 2009 2,500 1,250 1,250 5,000

31st March, 2010 2,500 1,250 1,250 5,000

Share of Profit*: 31st March, 2009 11,500 5,750 5,750 23,000

31st March, 2010 17,500 8,750 8,750 35,000

(Cr.) 34,000 27,000 17,000 78,000

(iii) Net Effect [(i) – (ii)] 8,000 Cr. 1,000 Cr. 9,000 Dr. ...

*Calculation of Share of Profit (31st March, 2009):

Adjusted Profits = ` 33,000 – ` 5,000 (Salary) – ` 5,000 (Interest on Capital) = ` 23,000

A’s Share = ` 23,000 × 2/4 = ` 11,500

B’s Share = ` 23,000 × 1/4 = ` 5,750

C’s Share = ` 23,000 × 1/4 = ` 5,750

Calculation of Share of Profit (31st March, 2010):

Adjusted Profits = ` 45,000 – ` 5,000 (Salary) – ` 5,000 (Interest on Capital) = ` 35,000

A’s Share = ` 35,000 × 2/4 = ` 17,500

B’s Share = ` 35,000 × 1/4 = ` 8,750

C’s Share = ` 35,000 × 1/4 = ` 8,750.