Page 45 - DEBKVOL-1

P. 45

Chapter 2 Accounting for Partnership Firms—Fundamentals 2.17

.

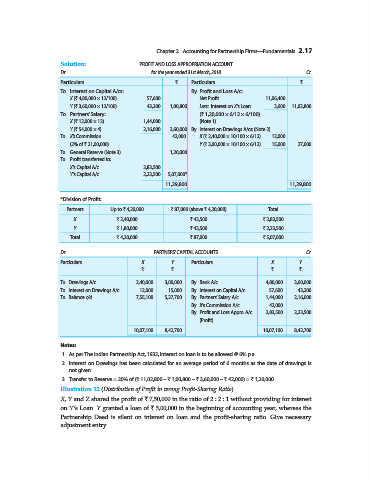

Solution: PROFIT AND LOSS APPROPRIATION ACCOUNT

Dr. for the year ended 31st March, 2018 Cr.

Particulars ` Particulars `

To Interest on Capital A/cs: By Profit and Loss A/c:

X (` 4,80,000 × 12/100) 57,600 Net Profit 11,06,400

Y (` 3,60,000 × 12/100) 43,200 1,00,800 Less: Interest on X’s Loan 3,600 11,02,800

To Partners’ Salary: (` 1,20,000 × 6/12 × 6/100)

X (` 12,000 × 12) 1,44,000 (Note 1)

Y (` 54,000 × 4) 2,16,000 3,60,000 By Interest on Drawings A/cs: (Note 2)

To X’s Commission 42,000 X (` 2,40,000 × 10/100 × 6/12) 12,000

(2% of ` 21,00,000) Y (` 3,00,000 × 10/100 × 6/12) 15,000 27,000

To General Reserve (Note 3) 1,20,000

To Profit transferred to:

X’s Capital A/c 2,83,500

Y’s Capital A/c 2,23,500 5,07,000*

11,29,800 11,29,800

*Division of Profit:

Partners Up to ` 4,20,000 ` 87,000 (above ` 4,20,000) Total

X ` 2,40,000 ` 43,500 ` 2,83,500

Y ` 1,80,000 ` 43,500 ` 2,23,500

Total ` 4,20,000 ` 87,000 ` 5,07,000

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X Y Particulars X Y

` ` ` `

To Drawings A/c 2,40,000 3,00,000 By Bank A/c 4,80,000 3,60,000

To Interest on Drawings A/c 12,000 15,000 By Interest on Capital A/c 57,600 43,200

To Balance c/d 7,55,100 5,27,700 By Partners’ Salary A/c 1,44,000 2,16,000

By X’s Commission A/c 42,000 ...

By Profit and Loss Appro. A/c 2,83,500 2,23,500

(Profit)

10,07,100 8,42,700 10,07,100 8,42,700

Notes:

1. As per The Indian Partnership Act, 1932, Interest on loan is to be allowed @ 6% p.a.

2. Interest on Drawings has been calculated for an average period of 6 months as the date of drawings is

not given.

3. Transfer to Reserve = 20% of (` 11,02,800 – ` 1,00,800 – ` 3,60,000 – ` 42,000) = ` 1,20,000.

Illustration 12 (Distribution of Profit in wrong Profit-Sharing Ratio).

X, Y and Z shared the profit of ` 7,50,000 in the ratio of 2 : 2 : 1 without providing for interest

on Y’s Loan. Y granted a loan of ` 5,00,000 in the beginning of accounting year, whereas the

Partnership Deed is silent on interest on loan and the profit-sharing ratio. Give necessary

adjustment entry.