Page 92 - DEBKVOL-1

P. 92

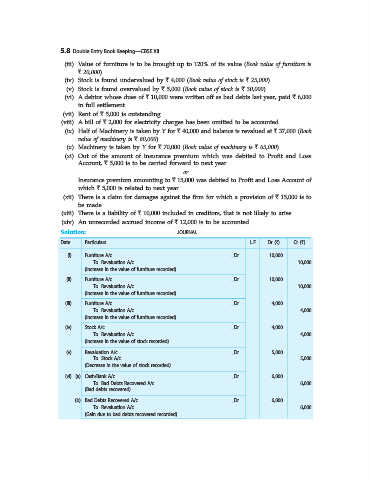

5.8 Double Entry Book Keeping—CBSE XII

(iii) Value of furniture is to be brought up to 120% of its value (Book value of furniture is

` 20,000).

(iv) Stock is found undervalued by ` 4,000 (Book value of stock is ` 25,000).

(v) Stock is found overvalued by ` 5,000 (Book value of stock is ` 30,000).

(vi) A debtor whose dues of ` 10,000 were written off as bad debts last year, paid ` 6,000

in full settlement.

(vii) Rent of ` 5,000 is outstanding.

(viii) A bill of ` 2,000 for electricity charges has been omitted to be accounted.

(ix) Half of Machinery is taken by Y for ` 40,000 and balance is revalued at ` 37,000 (Book

value of machinery is ` 80,000).

(x) Machinery is taken by Y for ` 70,000 (Book value of machinery is ` 65,000).

(xi) Out of the amount of insurance premium which was debited to Profit and Loss

Account, ` 5,000 is to be carried forward to next year.

or

Insurance premium amounting to ` 15,000 was debited to Profit and Loss Account of

which ` 5,000 is related to next year.

(xii) There is a claim for damages against the firm for which a provision of ` 15,000 is to

be made.

(xiii) There is a liability of ` 10,000 included in creditors, that is not likely to arise.

(xiv) An unrecorded accrued income of ` 12,000 is to be accounted.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

(i) Furniture A/c ...Dr. 10,000

To Revaluation A/c 10,000

(Increase in the value of furniture recorded)

(ii) Furniture A/c ...Dr. 10,000

To Revaluation A/c 10,000

(Increase in the value of furniture recorded)

(iii) Furniture A/c ...Dr. 4,000

To Revaluation A/c 4,000

(Increase in the value of furniture recorded)

(iv) Stock A/c ...Dr. 4,000

To Revaluation A/c 4,000

(Increase in the value of stock recorded)

(v) Revaluation A/c ...Dr. 5,000

To Stock A/c 5,000

(Decrease in the value of stock recorded)

(vi) (a) Cash/Bank A/c ...Dr. 6,000

To Bad Debts Recovered A/c 6,000

(Bad debts recovered)

(b) Bad Debts Recovered A/c ...Dr. 6,000

To Revaluation A/c 6,000

(Gain due to bad debts recovered recorded)