Page 96 - DEBKVOL-1

P. 96

5.12 Double Entry Book Keeping—CBSE XII

Illustration 9.

X and Y sharing profits in the ratio of 3 : 2 had the following Balance Sheet as at 31st

March, 2018:

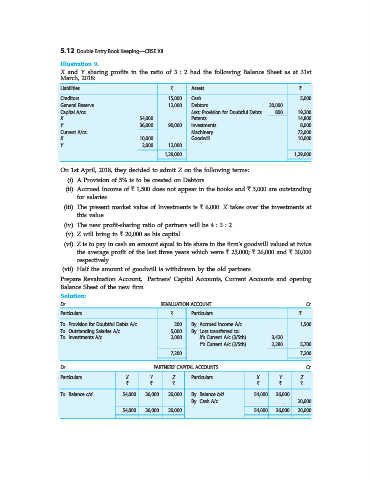

Liabilities ` Assets `

Creditors 15,000 Cash 5,000

General Reserve 12,000 Debtors 20,000

Capital A/cs: Less: Provision for Doubtful Debts 800 19,200

X 54,000 Patents 14,800

Y 36,000 90,000 Investments 8,000

Current A/cs: Machinery 72,000

X 10,000 Goodwill 10,000

Y 2,000 12,000

1,29,000 1,29,000

On 1st April, 2018, they decided to admit Z on the following terms:

(i) A Provision of 5% is to be created on Debtors.

(ii) Accrued Income of ` 1,500 does not appear in the books and ` 5,000 are outstanding

for salaries.

(iii) The present market value of Investments is ` 6,000. X takes over the investments at

this value.

(iv) The new profit-sharing ratio of partners will be 4 : 3 : 2.

(v) Z will bring in ` 20,000 as his capital.

(vi) Z is to pay in cash an amount equal to his share in the firm’s goodwill valued at twice

the average profit of the last three years which were ` 25,000; ` 26,000 and ` 30,000

respectively.

(vii) Half the amount of goodwill is withdrawn by the old partners.

Prepare Revaluation Account, Partners’ Capital Accounts, Current Accounts and opening

Balance Sheet of the new firm.

Solution:

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Provision for Doubtful Debts A/c 200 By Accrued Income A/c 1,500

To Outstanding Salaries A/c 5,000 By Loss transferred to:

To Investments A/c 2,000 X’s Current A/c (3/5th) 3,420

Y’s Current A/c (2/5th) 2,280 5,700

7,200 7,200

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars X Y Z Particulars X Y Z

` ` ` ` ` `

To Balance c/d 54,000 36,000 20,000 By Balance b/d 54,000 36,000 ...

By Cash A/c ... ... 20,000

54,000 36,000 20,000 54,000 36,000 20,000