Page 94 - DEBKVOL-1

P. 94

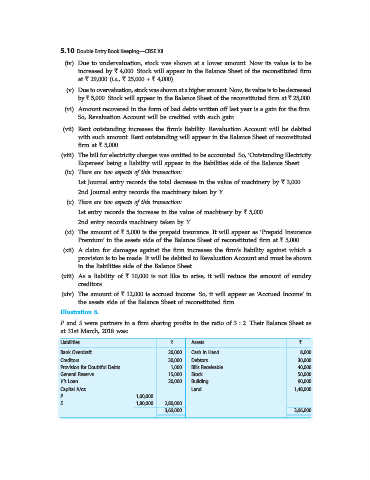

5.10 Double Entry Book Keeping—CBSE XII

(iv) Due to undervaluation, stock was shown at a lower amount. Now its value is to be

increased by ` 4,000. Stock will appear in the Balance Sheet of the reconstituted firm

at ` 29,000 (i.e., ` 25,000 + ` 4,000).

(v) Due to overvaluation, stock was shown at a higher amount. Now, its value is to be decreased

by ` 5,000. Stock will appear in the Balance Sheet of the reconstituted firm at ` 25,000.

(vi) Amount recovered in the form of bad debts written off last year is a gain for the firm.

So, Revaluation Account will be credited with such gain.

(vii) Rent outstanding increases the firm’s liability. Revaluation Account will be debited

with such amount. Rent outstanding will appear in the Balance Sheet of reconstituted

firm at ` 5,000.

(viii) The bill for electricity charges was omitted to be accounted. So, ‘Outstanding Electricity

Expenses’ being a liability will appear in the liabilities side of the Balance Sheet.

(ix) There are two aspects of this transaction:

1st Journal entry records the total decrease in the value of machinery by ` 3,000.

2nd Journal entry records the machinery taken by Y.

(x) There are two aspects of this transaction:

1st entry records the increase in the value of machinery by ` 5,000.

2nd entry records machinery taken by Y.

(xi) The amount of ` 5,000 is the prepaid insurance. It will appear as ‘Prepaid Insurance

Premium’ in the assets side of the Balance Sheet of reconstituted firm at ` 5,000.

(xii) A claim for damages against the firm increases the firm’s liability against which a

provision is to be made. It will be debited to Revaluation Account and must be shown

in the liabilities side of the Balance Sheet.

(xiii) As a liability of ` 10,000 is not like to arise, it will reduce the amount of sundry

creditors.

(xiv) The amount of ` 12,000 is accrued income. So, it will appear as ‘Accrued Income’ in

the assets side of the Balance Sheet of reconstituted firm.

Illustration 8.

P and S were partners in a firm sharing profits in the ratio of 3 : 2. Their Balance Sheet as

at 31st March, 2018 was:

Liabilities ` Assets `

Bank Overdraft 20,000 Cash in Hand 8,000

Creditors 30,000 Debtors 30,000

Provision for Doubtful Debts 1,000 Bills Receivable 40,000

General Reserve 15,000 Stock 50,000

V’s Loan 20,000 Building 90,000

Capital A/cs: Land 1,48,000

P 1,00,000

S 1,80,000 2,80,000

3,66,000 3,66,000