Page 412 - AAAXII

P. 412

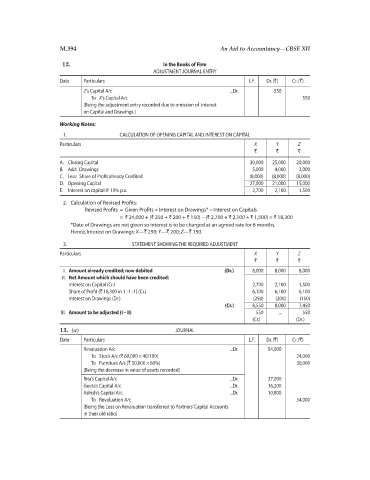

M.394 An Aid to Accountancy—CBSE XII

12. In the Books of Firm

ADJUSTMENT JOURNAL ENTRY

Date Particulars L.F. Dr. (`) Cr. (`)

Z’s Capital A/c ...Dr. 550

To X’s Capital A/c 550

(Being the adjustment entry recorded due to omission of interest

on Capital and Drawings )

Working Notes:

1. CALCULATION OF OPENING CAPITAL AND INTEREST ON CAPITAL

Particulars X Y Z

` ` `

A. Closing Capital 30,000 25,000 20,000

B. Add: Drawings 5,000 4,000 3,000

C. Less: Share of Profit already Credited (8,000) (8,000) (8,000)

D. Opening Capital 27,000 21,000 15,000

E. Interest on capital @ 10% p.a. 2,700 2,100 1,500

2. Calculation of Revised Profits:

Revised Profits = Given Profits + Interest on Drawings* – Interest on Capitals

= ` 24,000 + (` 250 + ` 200 + ` 150) – (` 2,700 + ` 2,100 + ` 1,500) = ` 18,300

*Date of Drawings are not given so interest is to be charged at an agreed rate for 6 months.

Hence, Interest on Drawings: X—` 250; Y—` 200; Z—` 150.

3. STATEMENT SHOWING THE REQUIRED ADJUSTMENT

Particulars X Y Z

` ` `

I. Amount already credited; now debited (Dr.) 8,000 8,000 8,000

II. Net Amount which should have been credited:

Interest on Capital (Cr.) 2,700 2,100 1,500

Share of Profit (` 18,300 in 1 : 1 : 1) (Cr.) 6,100 6,100 6,100

Interest on Drawings (Dr.) (250) (200) (150)

(Cr.) 8,550 8,000 7,450

III. Amount to be adjusted (I – II) 550 ... 550

(Cr.) (Dr.)

13. (a) JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

Revaluation A/c ...Dr. 54,000

To Stock A/c (` 60,000 × 40/100) 24,000

To Furniture A/c (` 50,000 × 60%) 30,000

(Being the decrease in value of assets recorded)

Rita’s Capital A/c ...Dr. 27,000

Geeta’s Capital A/c ...Dr. 16,200

Ashish’s Capital A/c ...Dr. 10,800

To Revaluation A/c 54,000

(Being the Loss on Revaluation transferred to Partners’ Capital Accounts

in their old ratio)