Page 115 - afs12

P. 115

Cash Flow Statement 5.15

2. Dr. PLANT AND MACHINERY ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 4,00,000 By Bank A/c (Sale) 34,000

To Gain (Profit) on Sale of Plant A/c 10,000 By Accumulated Depreciation A/c 16,000

(Statement of Profit & Loss) (Depreciation on Plant Sold)

To Bank A/c (Bal. Fig., being Purchase) 6,40,000 By Balance c/d 10,00,000

10,50,000 10,50,000

3. Dr. ACCUMULATED DEPRECIATION ACCOUNT Cr.

Particulars ` Particulars `

To Plant and Machinery A/c 16,000 By Balance b/d 60,000

(Transfer of Depreciation on Plant Sold) By Depreciation (Bal. Fig.) 52,000

To Balance c/d 96,000 (Statement of Profit & Loss)

1,12,000 1,12,000

4. Dr. INVESTMENTS ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 80,000 By Bank A/c (Sale) 28,000

To Gain (Profit) on Sale of Investment A/c 8,000 (` 20,000 + 40% of ` 20,000)

(Statement of Profit & Loss) By Balance c/d 90,000

To Bank A/c (Bal. Fig., being Purchase) 30,000

1,18,000 1,18,000

5. Interest on Debentures = (` 4,00,000 × 15/100) + (` 1,00,000 × 15/100 × 8/12) = ` 60,000 + ` 10,000 = ` 70,000.

6. Since dividend payment on preference shares has a priority over payment of interim dividend payment on equity

shares so payment of dividend on preference shares is implied.

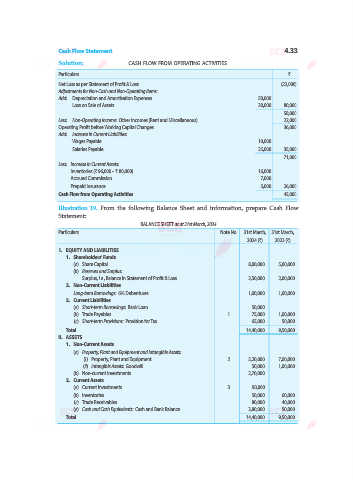

Illustration 10. Prepare Cash Flow Statement on the basis of information given in the

Balance Sheet of Simco Ltd. as at 31st March, 2025:

BALANCE SHEET as at 31st March, 2025

Particulars Note No. 31st March, 31st March,

2025 (`) 2024 (`)

I. EQUITY AND LIABILITIES

1. Shareholders’ Funds

(a) Share Capital 1 1,00,000 80,000

(b) Reserves and Surplus 2 10,000 6,000

2. Non-Current Liabilities

Long-term Borrowings 3 14,000 12,000

3. Current Liabilities

(a) Trade Payables 22,000 24,000

(b) Short-term Provisions 4 8,400 6,000

Total 1,54,400 1,28,000