Page 120 - afs12

P. 120

5.20 Analysis of Financial Statements—CBSE XII

Working Notes:

1. Dr. LAND AND BUILDING ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 6,50,000 By Bank A/c (Sale) 3,50,000

To Gain on Sale of Land and Building A/c 50,000 (Bal. Fig.)

(Statement of Profit & Loss) By Balance c/d 3,50,000

7,00,000 7,00,000

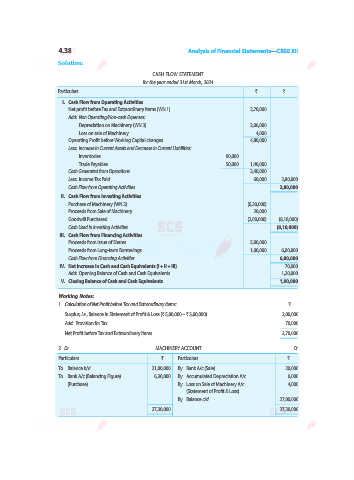

2. Dr. MACHINERY ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 2,75,000 By Depreciation A/c 27,500

To Bank A/c (Purchase) (Bal. Fig.) 4,77,500 By Balance c/d 7,25,000

7,52,500 7,52,500

Illustration12. From the following Balance Sheet of Essar Steel Ltd. as at 31st March, 2025,

prepare its Cash Flow Statement:

Particulars Note No. 31st March, 31st March,

2025 (`) 2024 (`)

I. EQUITY AND LIABILITIES

1. Shareholders’ Funds

(a) Share Capital 1 7,00,000 5,00,000

(b) Reserves and Surplus 2 2,50,000 3,25,000

2. Non-Current Liabilities

Long-term Borrowings 3 2,00,000 2,00,000

3. Current Liabilities

(a) Short-term Borrowings 4 ... 50,000

(b) Short-term Provisions 5 50,000 25,000

Total 12,00,000 11,00,000

II. ASSETS

1. Non-Current Assets

(a) Property, Plant and Equipment and Intangible Assets:

Property, Plant and Equipment (Machinery) 5,00,000 3,00,000

(b) Non-current Investments 2,00,000 1,40,000

2. Current Assets

(a) Inventories 1,50,000 2,00,000

(b) Trade Receivables 1,80,000 1,50,000

(c) Cash and Cash Equivalents 1,70,000 3,10,000

Total 12,00,000 11,00,000

Notes to Accounts

Particulars 31st March, 31st March,

2025 (`) 2024 (`)

1. Share Capital

Equity Share Capital 6,00,000 3,00,000

12% Preference Share Capital 1,00,000 2,00,000

7,00,000 5,00,000

2. Reserves and Surplus

General Reserve 1,50,000 3,75,000

Surplus, i.e., Balance in Statement of Profit & Loss 1,00,000 (50,000)

2,50,000 3,25,000

3. Long-term Borrowings

9% Debentures 2,00,000 2,00,000

4. Short-term Borrowings

Current Maturities of Long-term Debts (9% Debentures) ... 50,000

5. Short-term Provisions

Provision for Tax 50,000 25,000