Page 118 - afs12

P. 118

5.18 Analysis of Financial Statements—CBSE XII

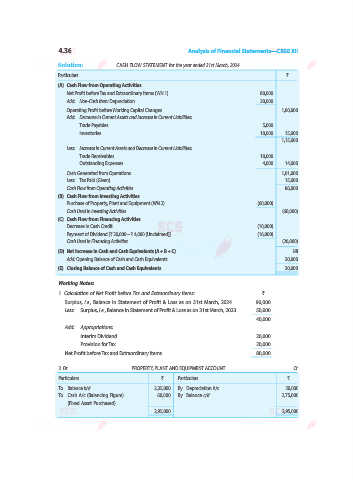

4. Dr. ACCUMULATED DEPRECIATION ACCOUNT Cr.

Particulars ` Particulars `

To Machinery A/c (Transfer) 6,000 By Balance b/d 22,000

To Balance c/d 30,000 By Depreciation A/c (Balancing Figure) 14,000

(Statement of Profit & Loss)

36,000 36,000

Illustration 11. From the following Balance Sheet of ABC Ltd., prepare Cash Flow Statement:

Particulars Note No. 31st March, 31st March,

2025 (`) 2024 (`)

I. EQUITY AND LIABILITIES

1. Shareholders’ Funds

(a) Share Capital 5,00,000 5,00,000

(b) Reserves and Surplus 1 2,75,000 1,50,000

2. Non-Current Liabilities

Long-term Borrowings 2 6,00,000 4,75,000

3. Current Liabilities

(a) Short-term Borrowings 3 75,000 50,000

(b) Trade Payables 1,75,000 1,00,000

(c) Short-term Provisions 4 1,25,000 1,00,000

Total 17,50,000 13,75,000

II. ASSETS

1. Non-Current Assets

Property, Plant and Equipment and Intangible Assets:

(i) Property, Plant and Equipment 5 10,75,000 9,25,000

(ii) Intangible Assets 6 25,000 37,500

2. Current Assets

(a) Inventories 2,50,000 1,37,500

(b) Trade Receivables 2,25,000 1,25,000

(c) Cash and Cash Equivalents 1,37,500 1,00,000

(d) Other Current Assets 7 37,500 50,000

Total 17,50,000 13,75,000

Notes to Accounts

Particulars 31st March, 31st March,

2025 (`) 2024 (`)

1. Reserves and Surplus

General Reserve 87,500 50,000

Surplus, i.e., Balance in Statement of Profit & Loss 1,87,500 1,00,000

2,75,000 1,50,000

2. Long-term Borrowings

10% Debentures 3,75,000 2,50,000

Mortgage Loan 2,25,000 2,25,000

6,00,000 4,75,000

3. Short-term Borrowings

Bank Overdraft 55,000 25,000

Cash Credit 20,000 25,000

75,000 50,000

4. Short-term Provisions

Provision for Tax 1,25,000 1,00,000