Page 13 - DEBK11

P. 13

Introduction to Accounting 1.3

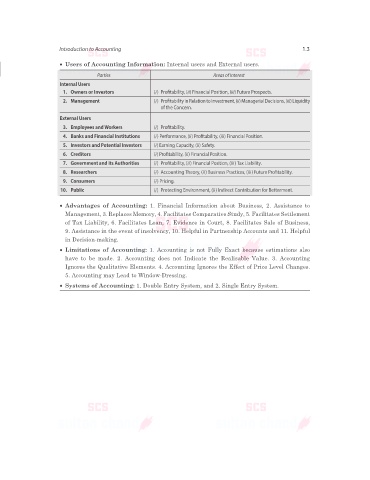

• Users of Accounting Information: Internal users and External users.

Parties Areas of Interest

Internal Users

1. Owners or Investors (i) Profitability, (ii) Financial Position, (iii) Future Prospects.

2. Management (i) Profitability in Relation to Investment, (ii) Managerial Decisions, (iii) Liquidity

of the Concern.

External Users

3. Employees and Workers (i) Profitability.

4. Banks and Financial Institutions (i) Performance, (ii) Profitability, (iii) Financial Position.

5. Investors and Potential Investors (i) Earning Capacity, (ii) Safety.

6. Creditors (i) Profitability, (ii) Financial Position.

7. Government and its Authorities (i) Profitability, (ii) Financial Position, (iii) Tax Liability.

8. Researchers (i) Accounting Theory, (ii) Business Practices, (iii) Future Profitability.

9. Consumers (i) Pricing.

10. Public (i) Protecting Environment, (ii) Indirect Contribution for Betterment.

• Advantages of Accounting: 1. Financial Information about Business, 2. Assistance to

Management, 3. Replaces Memory, 4. Facilitates Comparative Study, 5. Facilitates Settlement

of Tax Liability, 6. Facilitates Loan, 7. Evidence in Court, 8. Facilitates Sale of Business,

9. Assistance in the event of insolvency, 10. Helpful in Partnership Accounts and 11. Helpful

in Decision-making.

• Limitations of Accounting: 1. Accounting is not Fully Exact because estimations also

have to be made. 2. Accounting does not Indicate the Realisable Value. 3. Accounting

Ignores the Qualitative Elements. 4. Accounting Ignores the Effect of Price Level Changes.

5. Accounting may Lead to Window-Dressing.

• Systems of Accounting: 1. Double Entry System, and 2. Single Entry System.