Page 103 - DEBKVOL-1

P. 103

Chapter 5 Admission of a Partner 5.19

.

Prepare Revaluation Account, Partners’ Capital Accounts and Balance Sheet of the

reconstituted firm. (Delhi 2013, Modified)

Solution:

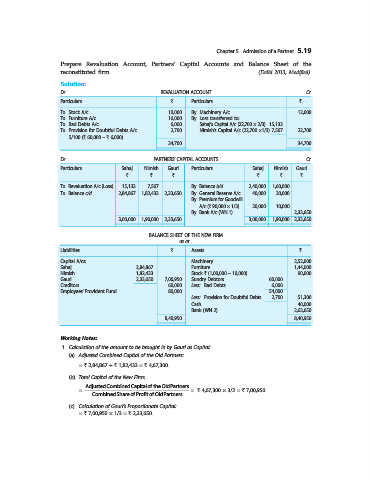

Dr. REVALUATION ACCOUNT Cr.

Particulars ` Particulars `

To Stock A/c 10,000 By Machinery A/c 12,000

To Furniture A/c 16,000 By Loss transferred to:

To Bad Debts A/c 6,000 Sahaj’s Capital A/c (22,700 × 2/3) 15,133

To Provision for Doubtful Debts A/c 2,700 Nimish’s Capital A/c (22,700 ×1/3) 7,567 22,700

5/100 (` 60,000 – ` 6,000)

34,700 34,700

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Sahaj Nimish Gauri Particulars Sahaj Nimish Gauri

` ` ` ` ` `

To Revaluation A/c (Loss) 15,133 7,567 ... By Balance b/d 2,40,000 1,60,000 ...

To Balance c/d 2,84,867 1,82,433 2,33,650 By General Reserve A/c 40,000 20,000 ...

By Premium for Goodwill

A/c (` 90,000 × 1/3) 20,000 10,000 ...

By Bank A/c (WN 1) ... ... 2,33,650

3,00,000 1,90,000 2,33,650 3,00,000 1,90,000 2,33,650

BALANCE SHEET OF THE NEW FIRM

as at...

Liabilities ` Assets `

Capital A/cs: Machinery 2,52,000

Sahaj 2,84,867 Furniture 1,44,000

Nimish 1,82,433 Stock ` (1,00,000 – 10,000) 90,000

Gauri 2,33,650 7,00,950 Sundry Debtors 60,000

Creditors 60,000 Less: Bad Debts 6,000

Employees’ Provident Fund 80,000 54,000

Less: Provision for Doubtful Debts 2,700 51,300

Cash 40,000

Bank (WN 2) 2,63,650

8,40,950 8,40,950

Working Notes:

1. Calculation of the amount to be brought in by Gauri as Capital:

(a) Adjusted Combined Capital of the Old Partners:

= ` 2,84,867 + ` 1,82,433 = ` 4,67,300.

(b) Total Capital of the New Firm:

Adjusted Combined Capital of the Old Partners

= = ` 4,67,300 × 3/2 = ` 7,00,950.

Combined Share of Profit of Old Partners

(c) Calculation of Gauri’s Proportionate Capital:

= ` 7,00,950 × 1/3 = ` 2,33,650.