Page 119 - DEBKVOL-1

P. 119

Chapter 5 Admission of a Partner 5.35

.

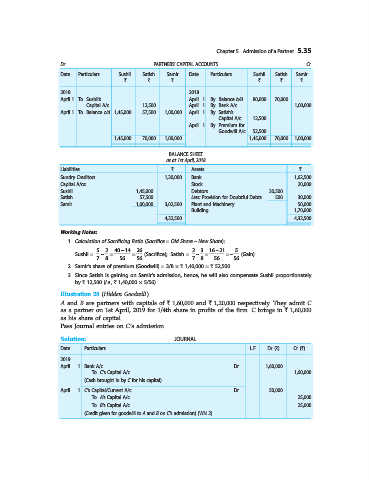

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Date Particulars Sushil Satish Samir Date Particulars Sushil Satish Samir

` ` ` ` ` `

2018 2018

April 1 To Sushil’s April 1 By Balance b/d 80,000 70,000 ...

Capital A/c ... 12,500 ... April 1 By Bank A/c ... ... 1,00,000

April 1 To Balance c/d 1,45,000 57,500 1,00,000 April 1 By Satish’s

Capital A/c 12,500 ... ...

April 1 By Premium for

Goodwill A/c 52,500 ... ...

1,45,000 70,000 1,00,000 1,45,000 70,000 1,00,000

BALANCE SHEET

as at 1st April, 2018

Liabilities ` Assets `

Sundry Creditors 1,30,000 Bank 1,62,500

Capital A/cs: Stock 20,000

Sushil 1,45,000 Debtors 30,500

Satish 57,500 Less: Provision for Doubtful Debts 500 30,000

Samir 1,00,000 3,02,500 Plant and Machinery 50,000

Building 1,70,000

4,32,500 4,32,500

Working Notes:

1. Calculation of Sacrificing Ratio (Sacrifice = Old Share – New Share):

5 2 40 -14 26 2 3 16 – 21 5

Sushil = - = = (Sacrifice); Satish = – = = – (Gain).

7 8 56 56 7 8 56 56

2. Samir’s share of premium (Goodwill) = 3/8 × ` 1,40,000 = ` 52,500.

3. Since Satish is gaining on Samir’s admission, hence, he will also compensate Sushil proportionately

by ` 12,500 (i.e., ` 1,40,000 × 5/56).

Illustration 28 (Hidden Goodwill).

A and B are partners with capitals of ` 1,60,000 and ` 1,20,000 respectively. They admit C

as a partner on 1st April, 2019 for 1/4th share in profits of the firm. C brings in ` 1,60,000

as his share of capital.

Pass Journal entries on C’s admission.

Solution: JOURNAL

Date Particulars L.F. Dr. (`) Cr. (`)

2019

April 1 Bank A/c ...Dr. 1,60,000

To C’s Capital A/c 1,60,000

(Cash brought in by C for his capital)

April 1 C’s Capital/Current A/c ...Dr. 50,000

To A’s Capital A/c 25,000

To B’s Capital A/c 25,000

(Credit given for goodwill to A and B on C’s admission) (WN 2)