Page 121 - DEBKVOL-1

P. 121

Chapter 5 Admission of a Partner 5.37

.

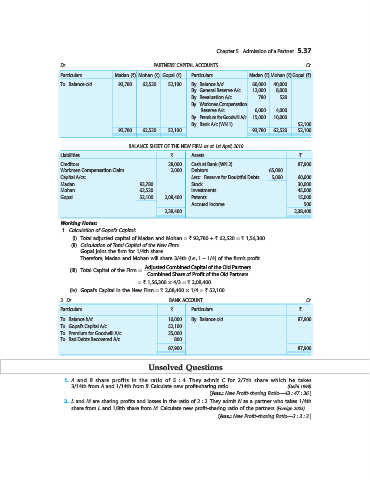

Dr. PARTNERS’ CAPITAL ACCOUNTS Cr.

Particulars Madan (`) Mohan (`) Gopal (`) Particulars Madan (`) Mohan (`) Gopal (`)

To Balance c/d 93,780 62,520 52,100 By Balance b/d 60,000 40,000 ...

By General Reserve A/c 12,000 8,000 ...

By Revaluation A/c 780 520 ...

By Workmen Compensation

Reserve A/c 6,000 4,000 ...

By Premium for Goodwill A/c 15,000 10,000 ...

By Bank A/c (WN 1) ... .... 52,100

93,780 62,520 52,100 93,780 62,520 52,100

BALANCE SHEET OF THE NEW FIRM as at 1st April, 2010

Liabilities ` Assets `

Creditors 28,000 Cash at Bank (WN 2) 87,900

Workmen Compensation Claim 2,000 Debtors 65,000

Capital A/cs: Less: Reserve for Doubtful Debts 5,000 60,000

Madan 93,780 Stock 30,000

Mohan 62,520 Investments 45,000

Gopal 52,100 2,08,400 Patents 15,000

Accrued Income 500

2,38,400 2,38,400

Working Notes:

1. Calculation of Gopal’s Capital:

(i) Total adjusted capital of Madan and Mohan = ` 93,780 + ` 62,520 = ` 1,56,300.

(ii) Calculation of Total Capital of the New Firm:

Gopal joins the firm for 1/4th share

Therefore, Madan and Mohan will share 3/4th (i.e., 1 – 1/4) of the firm’s profit.

Adjusted Combined Capital of the Old Partners

(iii) Total Capital of the Firm =

Combined Share of Profit of the Old Partners

= ` 1,56,300 × 4/3 = ` 2,08,400.

(iv) Gopal’s Capital in the New Firm = ` 2,08,400 × 1/4 = ` 52,100.

2. Dr. BANK ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 10,000 By Balance c/d 87,900

To Gopal’s Capital A/c 52,100

To Premium for Goodwill A/c 25,000

To Bad Debts Recovered A/c 800

87,900 87,900

Unsolved Questions

1. A and B share profits in the ratio of 5 : 4. They admit C for 2/7th share which he takes

3/14th from A and 1/14th from B. Calculate new profit-sharing ratio. (Delhi 1999)

[Ans.: New Profit-sharing Ratio—43 : 47 : 36.]

2. L and M are sharing profits and losses in the ratio of 2 : 2. They admit N as a partner who takes 1/4th

share from L and 1/8th share from M. Calculate new profit-sharing ratio of the partners. (Foreign 2003)

[Ans.: New Profit-sharing Ratio—2 : 3 : 3.]