Page 13 - DEBKVOL-1

P. 13

Chapter 1 Financial Statements of Not-for-Profit Organisations 1.3

.

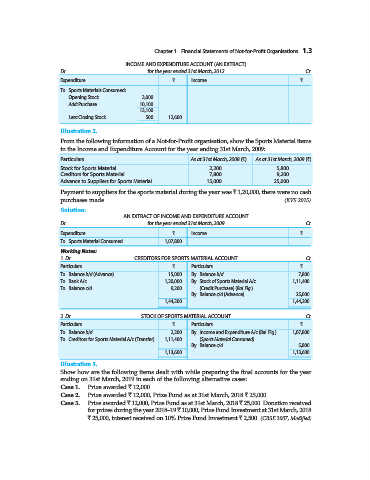

INCOME AND EXPENDITURE ACCOUNT (AN EXTRACT)

Dr. for the year ended 31st March, 2012 Cr.

Expenditure ` Income `

To Sports Materials Consumed:

Opening Stock 3,000

Add: Purchase 10,100

13,100

Less: Closing Stock 500 12,600

Illustration 2.

From the following information of a Not-for-Profit organisation, show the Sports Material items

in the Income and Expenditure Account for the year ending 31st March, 2009:

Particulars As at 31st March, 2008 (`) As at 31st March, 2009 (`)

Stock for Sports Material 2,200 5,800

Creditors for Sports Material 7,800 9,200

Advance to Suppliers for Sports Material 15,000 25,000

Payment to suppliers for the sports material during the year was ` 1,20,000, there were no cash

purchases made. (KVS 2015)

Solution:

AN EXTRACT OF INCOME AND EXPENDITURE ACCOUNT

Dr. for the year ended 31st March, 2009 Cr.

Expenditure ` Income `

To Sports Material Consumed 1,07,800

Working Notes:

1. Dr. CREDITORS FOR SPORTS MATERIAL ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d (Advance) 15,000 By Balance b/d 7,800

To Bank A/c 1,20,000 By Stock of Sports Material A/c 1,11,400

To Balance c/d 9,200 (Credit Purchase) (Bal. Fig.)

By Balance c/d (Advance) 25,000

1,44,200 1,44,200

2. Dr. STOCK OF SPORTS MATERIAL ACCOUNT Cr.

Particulars ` Particulars `

To Balance b/d 2,200 By Income and Expenditure A/c (Bal. Fig.) 1,07,800

To Creditors for Sports Material A/c (Transfer) 1,11,400 (Sports Material Consumed)

By Balance c/d 5,800

1,13,600 1,13,600

Illustration 3.

Show how are the following items dealt with while preparing the final accounts for the year

ending on 31st March, 2019 in each of the following alternative cases:

Case 1. Prize awarded ` 12,000.

Case 2. Prize awarded ` 12,000, Prize Fund as at 31st March, 2018 ` 25,000.

Case 3. Prize awarded ` 12,000, Prize Fund as at 31st March, 2018 ` 25,000. Donation received

for prizes during the year 2018–19 ` 10,000, Prize Fund Investment at 31st March, 2018

` 25,000, interest received on 10% Prize Fund Investment ` 2,500. (CBSE 2007, Modified)